Kwasi Ampofo, BNEF’s lead analyst covering battery raw materials, says China’s large scale investments into mining and refining has given it the advantage over Japan and Korea:

“Other countries seeking to be dominant players in the overall value chain may need to support upstream metals mining and refining development, while also formulating policies that will safeguard the environment.”

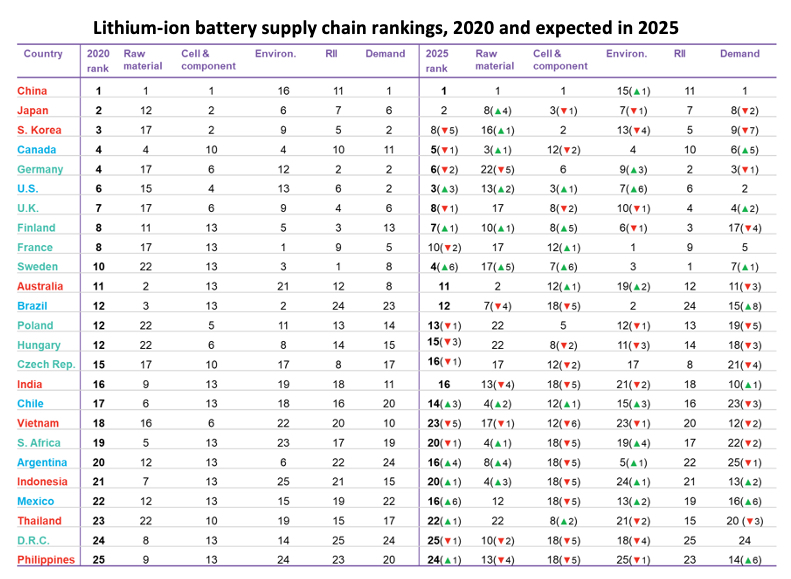

Canada, in fourth place, is boosted by its access to raw materials and environmental strengths but brought down by a relatively low score for regulation, infrastructure and innovation, and middling demand for batteries in electric vehicles and energy storage.

“Key distinguishing factors are the environmental footprint of industry, the availability of cheap but clean electricity, a technically skilled labor force, and incentives driving battery demand. These factors may be more important than a monopoly on one specific critical metal”

Sophie Lu, head of metals and mining at BloombergNEF

Currently at number 6, the US is forecast to slot in at number three by 2025, improving its metrics across the board.

James Frith, BNEF’s head of energy storage, says the next decade will be particularly interesting as Europe and the US try to create their own battery champions:

“While Europe is launching initiatives to capture more of the raw material value chain, the US is slower to react on this.”

BNEF says “if the US were to increase its investment in raw materials and promote EV adoption, it could overtake Japan and China to be number one in 2025.”

As EV demand grows there is an increasing need for cell manufacturing facilities close to automotive production. This has led to a boom in European cell plants, and the rest of the supply chain is also slowly making its way to Europe, according to the report.

The introduction of carbon border taxes as proposed by the European Commission and Joe Biden, the US Democratic presidential candidate, could give regions or countries leverage to secure localized supply chains.

Sophie Lu, head of metals and mining at BloombergNEF, says a key concern of many raw materials producing countries is how to leverage resource wealth into more value-add, and attract further downstream investments, like battery manufacturing:

“Key distinguishing factors are the environmental footprint of industry, the availability of cheap but clean electricity, a technically skilled labor force, and incentives driving battery demand. These factors may be more important than a monopoly on one specific critical metal.”