(Bloomberg) — The Western world’s largest oil explorers are sailing into earnings season on the tailwind of strong commodity prices after a 2020 they would rather forget.

With crude prices and refining margins buoyed by the rollout of Covid-19 vaccines and the prospect of an economic rebound, investors will be watching for signs in Big Oil’s fourth-quarter earnings that higher crude prices will translate into much-needed increased cash flows this year.

Some optimism is already priced in. Exxon Mobil Corp. and BP Plc, both of which last year weathered their worst stock-price slumps in decades, are up more than 10% in 2021. Still, the supermajors are largely out of favor: The combined market value of Exxon, Chevron Corp., Royal Dutch Shell Plc, Total SE and BP is now less than that of Tesla Inc.

The challenge for executives during conference calls with analysts and investors will be to strike the right balance between paying back debt, funding shareholder payouts and financing growth plans and energy-transition strategies.

Here are five things to watch for when they post fourth-quarter earnings, which are scheduled as follows:

1. Cash Generation

While higher commodity prices clearly benefit oil companies, the supermajors can be something of a black box in translating those gains into cash flows. Trading, production outages, cargo timing, refinery maintenance and fuel stockpiles can have an big impact on results. Investors will be watching for signs that strengthening prices are bolstering cash reserves.

The big oil drillers should be “outsized beneficiaries of the continued reopening trade,” Morgan Stanley analysts led by Devin McDermott wrote in a note to clients. But investors still need to see “visible cash flow” before turning bullish in the medium term.

The Morgan Stanley analysts believe cash flow is the single top indicator of stock performance for the supermajors as investors have largely given up on rewarding companies for boosting output, expanding underground reserves or timely project construction. The metric has become increasingly important as companies took on more debt.

2. Capital Allocation

All the supermajors aggressively cut spending in 2020 and investors will be wary of any moves to flex this year’s outlays higher in response to increasing prices, particularly in U.S. shale fields.

“After years of underperformance, for upstream oil & gas, 2021 can best be described as the proof of concept year,” Barclays Plc analysts led by Jeanine Wai wrote in a note. “The oil macro is arguably serving up free cash flow on a silver platter if management teams can just stay disciplined.”

Chevron Chief Executive Officer Mike Wirth will likely face questions around his appetite for further takeovers, given the company’s relatively strong balance sheet and recent $5 billion purchase of Noble Energy Inc. Meanwhile, Exxon executives will once again be asked about their ability to maintain the third-largest dividend in the S&P 500 Index.

For a look at Bloomberg Intelligence’s ESG data, click here

For BP and Shell, it will all be about shareholder returns. Both companies slashed dividends last year, drawing the ire of investors counting on generous payouts. Shell sought to woo some of them back during the third quarter with a modest dividend increase and the promise of further hikes as well as share buybacks as debt is reduced.

BP also has promised to return surplus cash to shareholders, but with more debt and bigger commitments to low-carbon spending, that is further down on their priority list.

The European majors have all promised – to differing levels – to ramp up investments into cleaner energy over the next decades. But oil and natural gas are still their bread and butter, meaning that they will have to juggle money flowing into fossil fuels while also diverting capital into less-profitable renewables and shareholder payouts.

3. Writedowns

Exxon’s fourth-quarter results will be marred by its biggest-ever writedown, which the company has warned may be as large as $20 billion. For its part, Shell warned in December of another multibillion-dollar impairment that will bring the tally for the year to more than $22 billion.

Shell expects more charges to come this year related to its global restructuring. The firm will cut as many as 9,000 jobs over two years, and has already announced 1,600 workforce reductions in its home countries of the Netherlands and U.K. Chief Financial Officer Jessica Uhl said in October that severance costs tied to the revamp would likely amount to $1.5 billion to $2 billion.

4. Demand Outlook

With their giant networks of refineries, terminals and filling stations, the oil majors have a unique insight into global demand patterns, the key signal for oil markets as the world copes with Covid-19. Executives’ comments on anticipated customer behavior will be closely scrutinized with a view to whether the recent price rally will be fleeting or the beginning of another commodity supercycle.

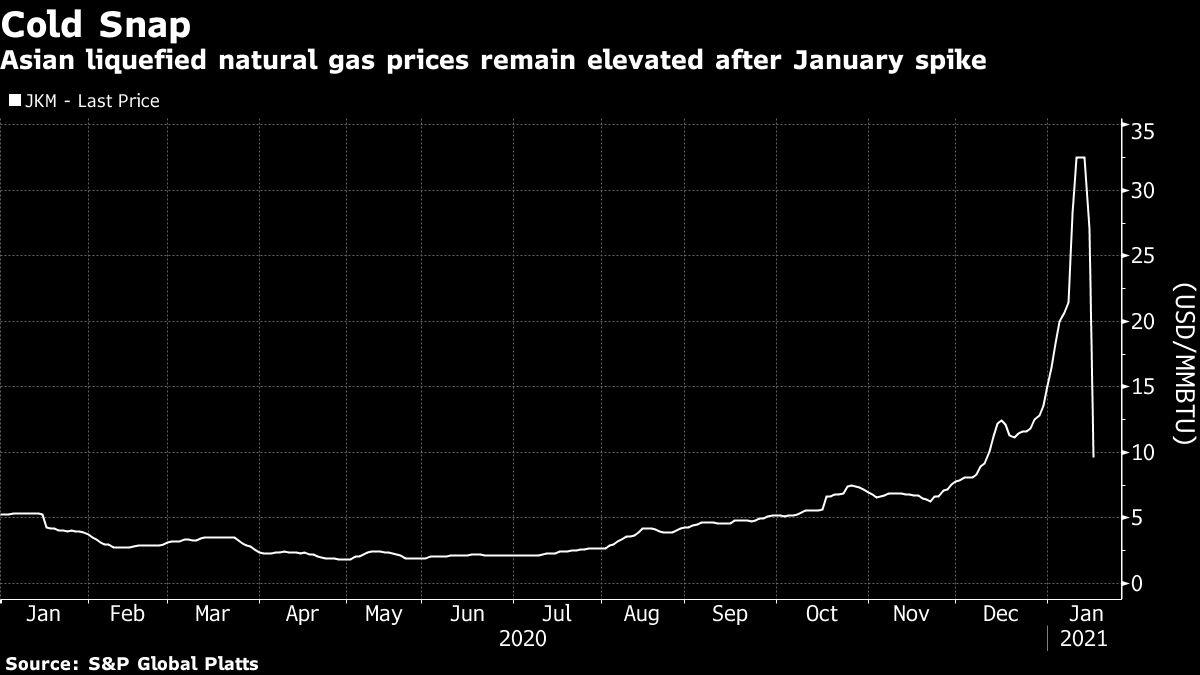

Of particular interest will be the outlook for liquefied natural gas in Asia, which saw a stunning price spike in recent weeks due to weather-driven demand for heating fuel. Though many long-term LNG contracts are benchmarked to the price of oil, the spot market is still an important indicator of demand.

5. Restructuring

The crisis of 2020 was so severe that the majors’ quickly resorted to huge layoffs to reduce costs, and now investors will want to see what kind of savings have been reaped. Exxon has already indicated it will beat its target of reducing operating expenses by 15%, and 14,000 job cuts also ought to lead to longer-term gains.

In Europe, Shell isn’t the only firm to slim down operations. BP said in June that it would reduce its 70,000-strong workforce by 10,000 to help ease $8 billion in annual “people costs.” BP CEO Bernard Looney has stressed that for the company to transition into cleaner energy it needs to be more nimble, and that has meant dismantling the traditional upstream and downstream divisions, and stripping away entire layers of management.

For more articles like this, please visit us at bloomberg.com

Subscribe now to stay ahead with the most trusted business news source.

©2021 Bloomberg L.P.