‘Buffett Indicator’ is alarmingly bearish and this year’s Berkshire shareholder letter could reveal why

Should investors continue to give Warren Buffett the benefit of the doubt?

That is the big question for Berkshire Hathaway BRK.A,

This question wouldn’t be so urgent if 2020 — when Berkshire stock lagged the S&P 500 SPX,

I have no idea whether Buffett will address the market-lagging performance of Berkshire stock in his letter or at the company’s annual meeting. My request for comment from the company has gone unanswered. But I would be surprised if he doesn’t address it, and in the rest of this column I want to provide some background information that will help us understand the significance of what he may have to say.

Will Buffett double down on his bearish stock market outlook?

Pay close attention to whether Buffett doubles down on the bearish posture with which he has approached the stock market in recent years. It’s largely because of that bearishness that Berkshire stock has lagged. At the beginning of last year’s third quarter, for example, the company was sitting on a huge pile of cash — $147 billion, in fact.

Given the company’s conservative posture, it wouldn’t take much of a drop in the overall market for Berkshire stock to once again be ahead of the S&P 500 over the trailing 15 years. In fact, I calculate that all it would take would be for the S&P 500 to perform at least 3% worse than the company’s stock, which is quite likely to occur in a bear market. During the 2007-2009 bear market that accompanied the Great Financial Crisis, for example, Berkshire stock beat the S&P 500 by a cumulative 15 percentage points.

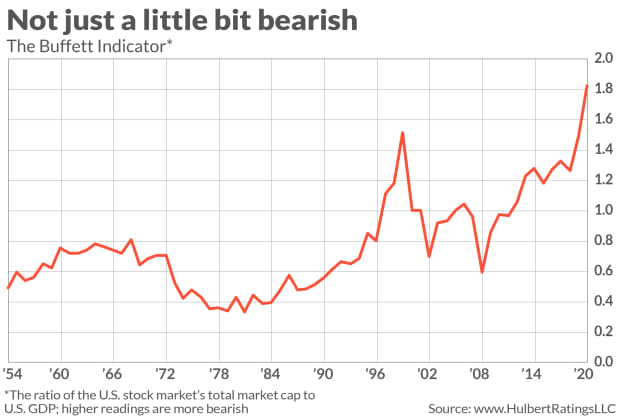

My guess is that Buffett will indeed double down on his bearishness. Consider the story told by the ratio of the stock market’s total market cap to U.S. GDP — the so-called Buffett Indicator. It got its name two decades ago when Buffett said that the ratio is “probably the best single measure of where valuations stand at any given moment.”

This ratio is now higher (and therefore more bearish) than at any other time in U.S. market history, higher even than where it stood at the top of the late 1990s internet bubble — as you can see from the chart below.

How big of a role has luck played?

Another big question as you decide whether to continue giving Buffett the benefit of the doubt: Could mere bad luck account for Berkshire’s market-lagging return? That’s an especially important question to ask, since the stock’s long-term record is nothing short of outstanding — even taking the past 15 years into account. Since 1965, Berkshire stock has outperformed the S&P 500 on a dividend-adjusted basis by the annualized margin of 20.1% to 10.2%. I’m aware of no other investor alive today who has come even close to doing as well as Buffett over this 56-year period.

To calculate the role luck may have played in performance, I conducted the following Monte Carlo simulation: What if, in each of the next 15 calendar years, Buffett’s alpha (return relative to the S&P 500) would be picked at random from his actual alphas over the past 56 years? And what if this experiment was run 10,000 times?

To put what I found in perspective, consider that Berkshire in fact has had negative alpha in five of the past 15 years. In 24.4% of my simulations, the company’s stock had negative alpha in at least that many years. One-out-of-four odds suggest there is nothing particularly unusual about the number of years in which the company’s stock actually has had negative alpha.

To be sure, it was less likely in my simulations for Berkshire to have a negative alpha over the entire 15-year period. But it still did happen — 2% of the time. So it’s possible that Buffett’s negative alpha over the past 15 years is due to nothing more than bad luck.

My vote is to continue to give Buffett the benefit of the doubt. There is no reason to pay less attention to his shareholder letter this year than in any prior year.

Mark Hulbert is a regular contributor to MarketWatch. His Hulbert Ratings tracks investment newsletters that pay a flat fee to be audited. He can be reached at mark@hulbertratings.com

More: Why Buffett’s shareholder letter is required reading for investors — and other CEOs