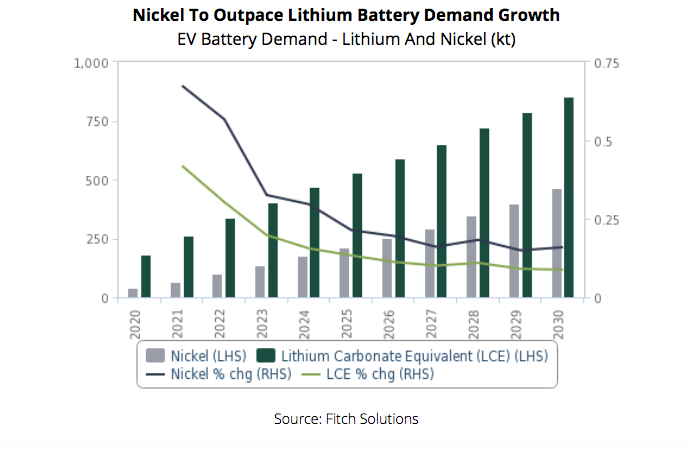

Fitch has updated its estimate of the impact of EV battery manufacturing on nickel consumption and now expects nickel demand for EV battery manufacturing to experience an annual average growth rate of 29% over 2021-2030, outpacing both lithium and cobalt demand, the analyst says.

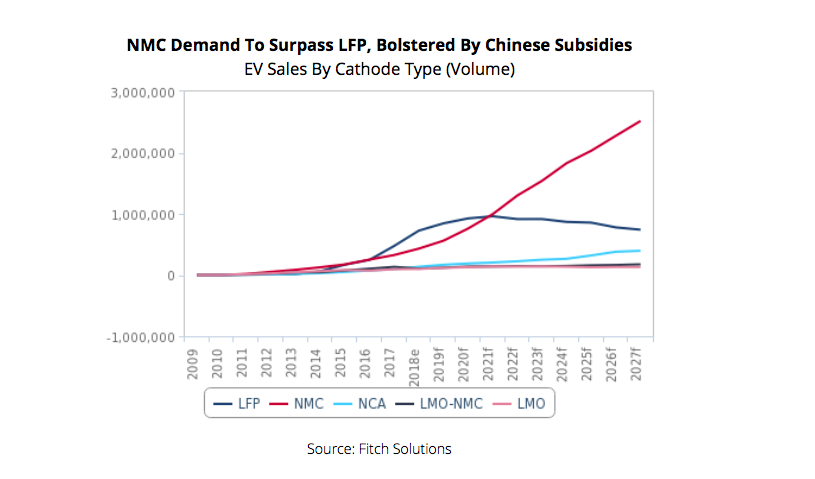

Fitch estimates of the impact of EV battery manufacturing on nickel demand rely on its 2018 forecasts for demand by cathode type, isolating demand for the lithium-nickel-manganese-cobalt oxide (NMC) chemistry, which it expects to be the preferred cathode of choice moving forward.

The analyst also maintains the underlying assumption that NMC 811 cathodes will rise to 80.0% of NMC market share by 2027, which will effectively raise the average nickel content from 34.6kg to 44.5kg for each NMC cathode produced.

Automakers such as BMW, Hyundai and Renault use the NMC chemistry in their vehicles, and Tesla currently employs a lithium-nickel-cobalt-aluminum oxide (NCA) chemistry in its models. Going forward, Fitch forecasts, Tesla will exchange its NCA chemistry for three different offerings based on vehicle cost and performance: lithium-iron-phosphate (LFP), NMC and a high-nickel, cobalt-free option.

Nickel demand will be supported by the metals persisting popularity in battery cathode chemistry, with downside risks caused by concerns over future supply availability, Fitch notes and expects nickel-dominant cathodes to be favoured for automakers’ heavy-duty and long-range vehicles.

However, Fitch says, a shortage of Class 1, battery-grade nickel may encourage automakers to explore lithium-iron-phosphate (LFP) batteries for mass-market vehicles.

(Read the full report here)