The new COVID relief bill has slashed Obamacare health-insurance premiums for early retirees

The American Rescue Plan Act of 2021 is a sweeping piece of legislation signed into law on March 11. The most highly publicized provision of the act is a third round of economic stimulus. Every eligible American will receive $1,400 for economic relief amidst the COVID-19 pandemic, if you haven’t received it already.

The act also substantially changes health-insurance premiums and subsidies for Marketplace plans. This has gotten far less press. It may have a bigger effect on many who need to bridge the gap from employer-provided health insurance to Medicare.

Overview of changes to the Affordable Care Act

Nearly everyone who purchases health insurance under the Affordable Care Act (ACA) Marketplace plans will benefit by the changes enacted as part of the American Rescue Plan Act of 2021. In summary:

- Early retirees with an income between 100% and 150% of the Federal Poverty Limit (FPL), who already paid little for health-insurance premiums, will now pay $0 premiums for silver-level plans.

- Those with incomes from 150% to 400% of FPL will see substantial reductions in health-insurance premium costs.

- Those with incomes that exceed 400% of FPL will no longer be subject to the ACA “subsidy cliff.” Health-insurance premiums costs will be capped at 8.5% of income.

- Older early retirees approaching Medicare age will benefit the most because costs rise as we age.

That’s good news across the board for early retirees who need to purchase medical insurance through Marketplace exchanges to bridge the gap from employer-provided coverage to Medicare. Let’s look at the details and discuss the implications for early retirement planning.

Decreased ACA premiums under the American Rescue Plan

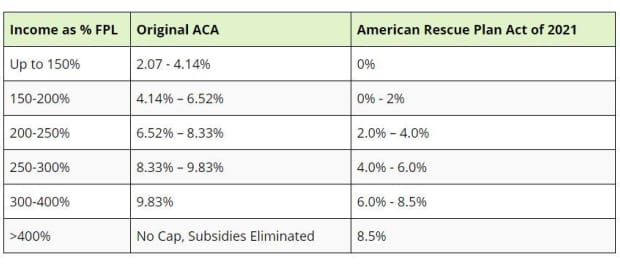

Part 7 of this Act reduces the maximum amount as a percentage of income, technically Modified Adjusted Gross Incomes (MAGI), that individuals or households will pay for health-insurance premiums.

The changes in the maximum percentage of household income paid for Silver Health Plan insurance premiums under the Original ACA and American Rescue Plan Act of 2021 are summarized here:

In a previous post, I explored Navigating ACA Tax Credits to Purchase Affordable Health Insurance In Early Retirement. It’s helpful to review a few scenarios I ran under the original ACA. I’ll then compare the scenarios under the new law.

Before and after premiums for low-income early retirees (under 150% of FPL)

In my previous article, I shared how early retirees can control taxable income through some combination of frugal living and/or generating income that doesn’t count toward MAGI. They could purchase quality health insurance through ACA exchanges at very favorable rates. This is accomplished by receiving large premium tax credits due to having low incomes. Premium tax credits are equal to the total cost of the premium minus the individual’s or household’s required contribution.

I showed that a household with an income at 138% of the FPL was required to pay only 3.42% of their income toward health-insurance premiums. In that scenario, the household would have paid $82 a month ($982 per year) for premiums. They would have received $1,320 per month ($15,836 per year) in premium subsidies.

Under the new law, things get even better for people in this scenario. They now would pay $0 toward health-insurance premiums. Subsidies would cover 100% of the cost.

Before and after premiums for very early retirees with 150% to 400% of FPL

When I wrote the previous article in November 2018, I entered our household scenario. We have two adults in our early 40s, one young child and estimated MAGI of $60,000. That income put us at 289% of the FPL for a household of three in 2018. We would pay 9.52% of our household income for medical-insurance premiums under the original ACA.

In 2021, unsubsidized health-insurance premiums would cost $14,358 for our family of three. I increased our household income to $62,750 to adjust for the slightly higher 2021 FPL to get us to the equivalent 289% of FPL. Under the old law, we would pay $498 a month ($5,974 per year) in premiums. We would qualify for a subsidy that would cover the remainder, amounting to $696 per month ($8,384 per year).

I ran our scenario under the new law with the Kaiser Health Insurance Calculator. For an apples-to-apples comparison, I kept income at 289% of the slightly higher 2021 FPL amount.

Under the new law, we would pay 5.56% of our income toward premiums. Our premiums would cost $291 a month ($3,489 per year), and we would receive a subsidy of $906 per month ($10,869 per year) to cover the remainder.

This change would save us about $207 each month ($2,485 per year). We would pay about 40% less for health-insurance premiums under the new law.

Before and after premiums for 60-year-old early retirees at 150% to 400% of FPL

Age is one of the few factors that impact premium costs with ACA plans. The older you are, the more expensive your premiums. As a comparison to our family, I created a scenario of an early retired couple in their early 60’s.

Unsubsidized health-insurance premiums for a 60-year-old couple (assuming children are grown and off the parents’ insurance) would cost $22,975 in 2021. For a household of two, the same 289% of FPL would be $50,344. This income number is lower than the above scenario because FPL is adjusted based on household size.

At 289% of FPL, they would pay 9.52% of income under the old law. Their share of the premiums would cost $399 each month ($4,793 per year). Their subsidy would be $1,515 a month ($18,182 per year).

Under the new law they would pay 5.56% of income. Their share of premiums under the new law would fall to $233 a month ($2,799 per year), and their subsidy would now be $1,681 per month ($20,176 per year)

The changes in the American Rescue Plan would save this couple in their early 60’s $166 each month ($1,994 per year). They would also pay about 40% less for health-insurance premiums than they would under the original ACA.

Elimination of the ACA subsidy cliff

The second, and potentially far more important, change that the American Rescue Plan Act of 2021 makes to the ACA is eliminating the “subsidy cliff.” Under the original law, if your MAGI exceeds 400% of the FPL, you lose premium subsidies completely.

Earning a single dollar of additional income at the 400%-of-FPL threshold could result in paying thousands of dollars in additional health-insurance premiums. Your subsidies would drop to zero.

With the change in the new law, the maximum anyone will pay for health-insurance premiums is 8.5% of their income. If your income exceeds 400% of FPL, you won’t lose thousands of dollars in premium subsidies. Instead, you will pay $8.50 more per year in premiums for every $100 of extra income you earn.

Eventually, the highest earners will lose subsidies completely and will have to pay the full cost. However, it is a gradual sliding scale down to zero subsidy.

Numbers better demonstrate the impact this new law will have on early retirees whose income just exceeds the 400% FPL threshold. Let’s dive in…

Premiums at the subsidy cliff for very early retirees

In my earlier post on ACA subsidies, I showed how a $100 difference in annual earnings at the 400%-of-FPL threshold would impact us. In that scenario, earning an additional $100 caused premium subsidies to drop off “the cliff” from $683 per month ($8,194 per year) to $0.

A similar scenario under the new law produces a much less dramatic result. An income of $86,700 puts us at 399% of FPL in 2021. At this level of income, our premiums would cost $613 each month ($7,352 per year). Our subsidy would be $652 per month ($7,825 per year). Subsidies would cover a little over half of our total $15,177 premiums cost.

Under the original ACA, we would have paid 9.83% of income toward our premiums. The new law saves us almost $1,000 in this scenario.

Bumping income up to $87,000 puts us at 401% of FPL. At this level of income, our premium cost rises a few dollars to $616 a month ($7,395 per year) while our premium subsidy drops a few dollars to $649 a month ($7,782 per year).

Under the old law we would pay the full unsubsidized cost of $15,177. This is about double what we would owe under the new law.

Under the American Rescue Plan, a small difference in income equates to a small increase in health insurance premiums and decrease in premium credits. This makes planning more predictable and less punitive if you make a small mistake around the 400%-of-FPL cutoff point.

Premiums at the subsidy cliff for 60-year-old retirees

Medical-insurance premiums increase as we age. This new law is most impactful for early retirees approaching Medicare eligibility who are over the 400%-of-FPL cliff. Let’s look at one last example.

Returning to a couple of 60-year-olds, their unsubsidized insurance premium would be approximately $1,880 per month ($22,563 per year).

Entering an income of $68,800 for this household of two puts them at 399% FPL. The American Rescue Act caps the amount a household pays for health insurance premiums at 8.5% of income. Under the original ACA they would have paid 9.83% of income.

This couple would pay premiums of $486 per month ($5,834 per year) under the new law with subsidies of $1,394 a month ($16,729 per year). Lowering the cap that a person at this income must pay decreases the premium by about $1,000 each year compared with the old law.

Increasing income to $69,100 pushes this couple to 401% of FPL. Their premiums under the new law will cost $489 each month ($5,874 per year). Their premium subsidy is $1,391 per month ($16,689 per year). Under the original ACA, they would have lost this entire subsidy by exceeding the “subsidy cliff” by a few dollars.

The new law produces a staggering saving of about $17,000 for this couple.

The American Rescue Plan Act of 2021 clearly benefits early retirees buying Marketplace health-insurance plans. Still, there’s a major problem for early retirement planning.

Planning implications

The American Rescue Plan Act of 2021 explicitly states that the changes to ACA subsidies are applicable only in the 2021 and 2022 tax years. What happens beyond that? No one knows for sure.

If you haven’t made a decision for this year, or would like to change your plan, there is a Special Enrollment Period through May 15, 2021.

For households like ours who plan year to year, learning of this retroactive change three months into the year is not helpful for 2021. We’ve already decided last December that Kim will continue to work enough so that we are getting our insurance through her employer through at least this December.

We still have 20-plus years until we’re both eligible for Medicare. We have at least a decade when we’re also responsible for our child’s health insurance. Without clarification on what happens to this law long term, we could theoretically pay anywhere from $0 to $15,000 for annual healthcare premiums. Those numbers don’t account for additional expenses if we actually need to receive medical care. They also don’t account for the facts that healthcare costs tend to inflate faster than the general inflation rate and premiums will get more expensive as we age.

Health insurance is still the big wild card in early retirement planning. We may not have enough saved to sustain an early retirement. Alternatively, we may have already saved too much. It’s a massive challenge to plan for something as important to your retirement success or failure as medical insurance. The rules can change at any time.

What to do?

For early retirees who are within a few years of Medicare eligibility, the American Rescue Plan is a game changer. It can potentially save you tens of thousands of dollars in anticipated health-insurance premiums over the next two years. This can bridge the gap to more predictable retirement healthcare expenses.

Long-term planning (defined as beyond 2022) of medical insurance for early retirement still requires assessing which way the political winds are blowing. This is always dangerous. We shouldn’t place too much stock in any plan that requires our predictions to be correct.

In 2016, presidential candidate Donald Trump ran on the promise to “repeal and replace” the ACA. President Trump, with Republicans controlling both the House and Senate, failed to do so. So it seems that some version of the ACA will be around for the foreseeable future.

Under the new Biden administration with a Democratic House and Senate, there is a clear will to expand the ACA or create new government health-insurance options. The politics and economics are complicated.

This new legislation is in effect for only two years. There will be a midterm election then. The political winds may shift again.

Our household will continue to remain flexible. I’m of the opinion that we are not truly financially independent until our investments can produce enough income to pay our full unsubsidized healthcare costs. Being financially independent while being dependent on unpredictable government subsidies for something so important seems like an oxymoron.

Chris Mamula retired from a career as a physical therapist at age 41. This was first published as “Does the American Rescue Plan Change Health Care Planning for Early Retirees?” on the blog “Can I Retire Yet?”

More by Chris Mamula on MarketWatch

I ran the tax numbers for a semi-retired life, and they look amazing