(Bloomberg) — Index funds are supposed to cut out the human-driven craziness that periodically infects markets, but the recent meme-stock fever proved the $11 trillion industry is far from immune.

The remarkable surge in shares of AMC Entertainment Holdings Inc. and a handful of other stocks is showing up in multiple exchange-traded funds, skewing portfolios, altering risk profiles and exerting outsized influence on prices.

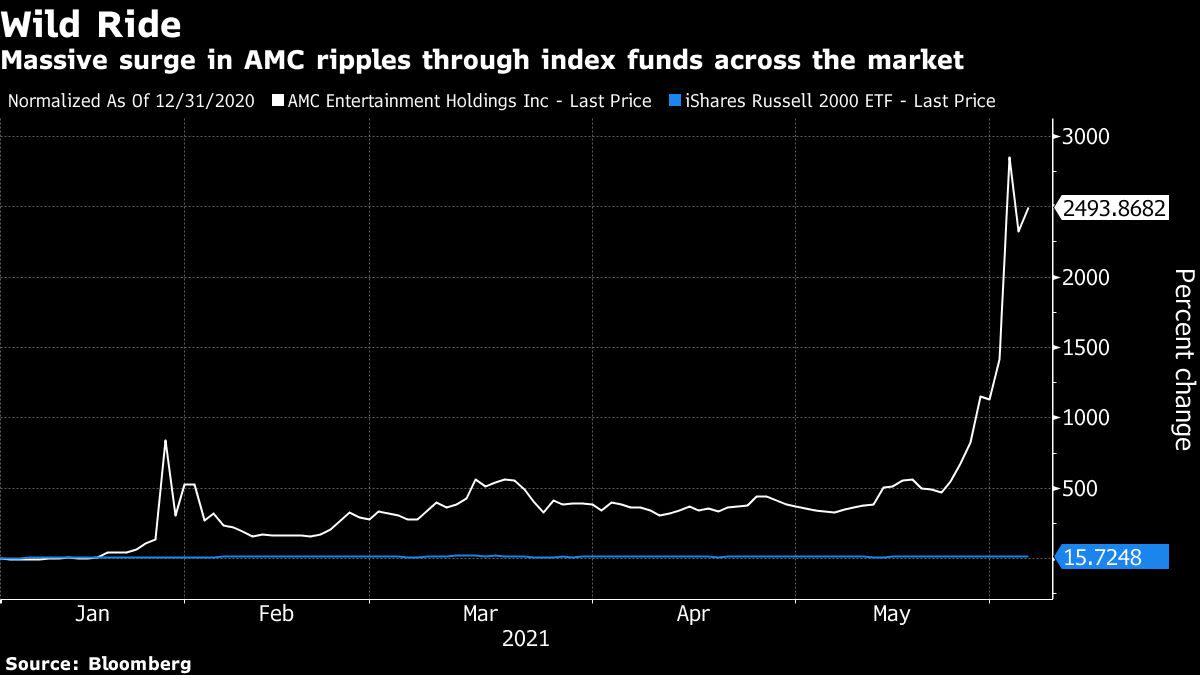

Take the $68 billion iShares Russell 2000 ETF (ticker IWM). In the past week through Thursday, AMC powered 70% of the product’s advance. The stock was responsible for less than a 10th of the fund’s return in the previous week.

It’s a timely reminder that even diversified funds on autopilot remain subject to the whims and eccentricities that frequently lash markets out of nowhere.

“For index investing, the appeal is that human decision-making, human emotions are taken out of it,” said Tom Essaye, a former Merrill Lynch trader who founded “the Sevens Report” newsletter. “That works all well and good until a stock that is supposed to be 50 basis points of the fund now becomes 6%.”

The AMC effect can be seen across a range of funds. Alongside IWM, the $17.5 billion iShares Russell 2000 Value ETF (IWN) and $72 billion iShares Core S&P Small-Cap ETF (IJR) have also seen the stock’s influence climb.

A similar phenomenon took place in January, when GameStop Corp. at one point surged more than 1,600%. Shares of the video-game retailer also rallied alongside AMC in the past week. The two companies are among a handful of shares dubbed meme stocks that are enjoying rapid, social-media fueled gains.

“Once the rules have been drawn up in the land of indexing, once the play has been called in the huddle, you don’t have that discretion,” said Ben Johnson, Morningstar’s global director of ETF research. “You take whatever the market is going to give you and execute the plays.”

Read more: Robinhood, Meme Stocks and Investing as a Game: QuickTake

The difference now is that investors have poured billions of dollars into products tracking smaller and cheaper stocks in the past six months, part of a broad rotation into more growth-sensitive companies to ride an economic recovery from Covid-19.

At the same time, meme mania is bigger than ever. Alongside AMC and GameStop, companies including BlackBerry Ltd., Koss Corp. and Bed Bath & Beyond Inc. also saw huge moves in the past week.

“Even in a basket of 2,000 stocks you’re getting some systemic risk around this concept of retail meme stocks because they’re small enough to push around,” said Nick Colas, co-founder of DataTrek Research.

Balancing Act

The cash and chaos exposes a glitch in the plumbing of many funds, which is that they’re often tied to the rebalancing schedule of the index they follow.

Given the speed of the rallies in the likes of AMC and GameStop, even tracking an index that rebalances quarterly — a relatively frequent schedule, by industry standards — leaves a fund susceptible to distortion.

One of the most-dramatic examples occurred in May, though it was unrelated to the meme-fueled drama. Around 68% of the $14.5 billion iShares MSCI USA Momentum Factor ETF (MTUM) had to be changed because of the huge market rotation that occurred since its last semiannual rebalance.

For quants who like to slice and dice stocks by characteristics like how expensive they appear or how much their prices swing around — known as factors — it’s all known as style drift. The fund is drifting away from its strategy, or investing style.

Not too long ago, AMC shares looked cheap and beaten down, meaning it qualified for many value factor strategies. But the wild surge of recent weeks makes it among the most-expensive stocks in the Russell 3000.

AMC shares currently stand at almost 10 times the level analysts see it trading a year from now: $5.25. The premium tops all Russell 3000 stocks that have enough of an analyst following to generate a price target, according to Bloomberg data, and more than double that of GameStop — the next over-valued stock.

AMC will likely remain in many value funds until their rebalancing comes around.

“Research tells premiums such as those associated with small cap and value stocks are generally delivered by a subset of the asset class,” said Wes Crill at Dimensional Fund Advisors, a pioneer of quant investing which has $637 billion under management. “Style drift can reduce the odds of capturing the premiums when they appear.”

The obvious solution would be to rebalance more often. But that would bring more transactional costs to funds, which can be a big problem for passive vehicles charging rock-bottom fees.

For some, the timing works out, merely by happenstance. AMC made up 21% of the $1.8 billion Invesco Dynamic Leisure and Entertainment ETF (PEJ) at one point on Wednesday. Thanks to its regularly scheduled rebalancing, it had zero shares of AMC by Friday.

Pickers’ Delight

Indexes are created using all sorts of methods, but the most common are cap-weighted and equal-weighted. And neither is immune to meme-stock distortion.

IWM is based on a cap-weighted index, meaning it allocates according to a company’s market cap. While that means it can keep pace with AMC’s rally, it’s automatically more exposed to potentially unstable investments. The fund now holds 1.75% of AMC, Bloomberg data show.

At the other end of the spectrum, the $21 million SoFi 50 ETF (SFYF) is based on an equal-weight gauge, meaning it aims to hold roughly the same value of shares in each of its constituents. But with a semiannual rebalancing schedule, AMC now accounts for 20% of the fund. It should be in the low single digits.

Read more: AMC Is Hijacking a Tiny Meme ETF as Weighting Grows 4% an Hour

Ultimately, all of this should add up to good news for active money managers.

While lumbering index funds are at the mercy of meme-mania and the rebalancing schedule, stock pickers can move fast to exploit extreme market action.

“If there are parts of the market that have been hijacked and pushed higher by retail investors, perhaps just avoiding those will provide active managers the ability to outperform in the coming years,” said Brent Schutte, chief investment strategist at Northwestern Mutual Wealth Management Company.

More stories like this are available on bloomberg.com

Subscribe now to stay ahead with the most trusted business news source.

©2021 Bloomberg L.P.

Shares?")