Champagne supercycle: Taking the fizz out of the commodities price boom

Scots may be known for their frugality, but at this website we don’t believe in taking the fizz out of anything so we decided to get on the wagon and take another look at Woodmac’s GET and planet decarbonisation predictions.

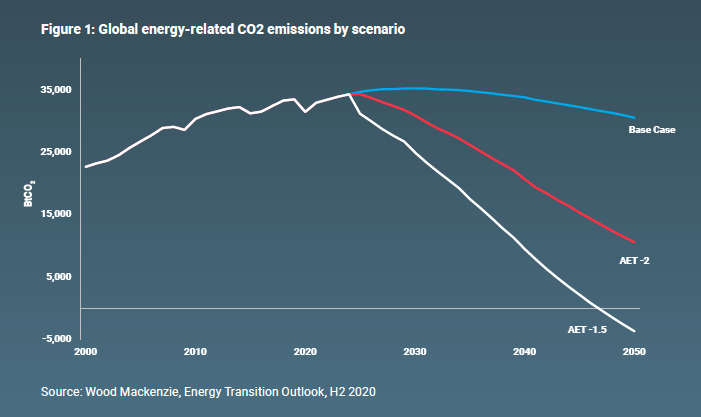

Under Woodmac’s most aggressive scenario for cutting the world’s carbs (like a strict keto diet – you’re not allowed beer, only Scotch), Morris says $50 trillion must be invested by 2050 “to electrify infrastructure and engineer out the aspects of modern life that most significantly contribute to carbon emissions”.

$50 trillion certainly looks and quacks like a supercycle duck (or on current trajectory the combined worth of Bezos/Scott, Musk/c and Gates/French in 2050) and miners would be pleased as punch for even a snifter of that, considering the dregs the industry has had to be content with in the past.

But Morris warns not to pop the corks just yet.

While the report does say “a supercycle is coming,” it’s not here yet, and overall the Morris metals and mining message is a sobering one – essentially saying mining and metals pundits are already drinking, but the party hasn’t started.

Designated drivers

Morris says decarbonisation creates “as many risks as opportunities” (Morris ran due diligence for Rio Tinto before joining Woodmac so circumspection may be expected).

The sweeping paper lays out the many ways the GET-induced supercycle could see miners sipping sovetskoye shampanskoye instead of downing Dom Perignon:

One, China. China rules over swathes of the mining world, especially the battery metals supply chain, but “its aspirations have not yet been satisfied and we expect its control to continue to grow,” says Morris:

“Those who choose to participate too late in the cycle – be they nations seeking to secure supply for themselves, customers wanting to protect their production lines or investors wanting to cash in on supernormal profits – are likely to find that they either can’t afford to participate or are precluded altogether.”

Delirium tremens

Two, systemic supply uncertainty. Under Woodmac’s mid-range net-zero by 2070 scenario (keto, but with pizza and beer on weekends) the required installed capacity becomes “eye-watering”.

But they will not be tears of joy, because “if consumption patterns and the metal processing technologies used today endure over the coming decades, the disconnect between supply capability and demand will become almost inconceivably large, under any scenario.”

In agreement so far with Woodmac’s thesis but not so sure about the third fizzle factor – a new generation of green consumers turning against miners.

Morris says electric vehicles would be the single most impactful driver of metals demand, but both carmakers and miners are faced with the rise of “consumption consciousness”.

“Whipping up a frenzy over the dizzying levels of additional metal” needed to feed the GET over the next 20 years “could prove a Pyrrhic victory,” says Morris.

“If metals producers are too successful in drawing attention to how much of their primary (that is, non-recycled) metal will go into cars, phones, telecoms and energy transition infrastructure, they may find themselves the new target of consumers’ ire.”

Battery lives

Not sure about this contention, have you ever tried to come between a gen Z (and to be fair gen Y and X too) and his/her/their/zir’s phone?

We’ll crawl over non-recycled broken glass for the next Tiktok, swim through deep sea tailings to Insta, climb leach heaps to become Youtubers and drink slurry to binge Netflix.

Ground zero for consumption consciousness over battery metals would be the cobalt–Congo–China chain, but the billion iphone users in the world care whether their battery is going to run out before the next Star Wars meme loads, not who dug out the Co with bare hands.

No-one reads the terms and conditions of social media networks or mobile phone apps, much less Facebook, Google or Apple’s Form SD on conflict minerals.

Generalized range anxiety disorder

Morris warns about increasing thrifting and substitution if the reduce, reuse and recycle people heroes see too much fresh metal coming out of too many new holes.

It may also lead them to “conceivably switch off more fully from some types of consumption”:

“For instance, if the ‘Uberfication’ of private transport drove a switch to pooled rather than individual vehicle ownership, cutting car consumption, metals demand will suffer.”

Fair point, until the average conscious consumer is stranded next to the road because the government banned all ICE cars, the shared electric car is an LFP because of thrifting by underpaid Uber drivers, and not enough copper was recycled to build the charging stations.

At this stage of the GET – best bet circa 2030 – there’s no amount of nickel-cobalt-manganese mining the average conscious consumer will not allow.

And if the next mining supercycle is to be a Pyrrhic victory as Morris says, it sure shouldn’t be because not enough cobalt in the batteries caused thermal runaway.

Mining is the aperitif, not the main course

While Leonardo Dicaprio’s Rhodesian accent was admirable, Blood Diamond was forgettable, Matthew McConaughey’s Gold was small beer and Avatar was just silly (not just the use of Papyrus but the word “unobtanium”. Come on).

Chinese rare earths is the one mining narrative that caught the imagination of the broader public, albeit briefly, becoming the basis of a best-selling video game and a plot point in a once top-rated Netflix series.

Ten years ago: Chinese control of rare earths sparks a world war and millions of hours are spent by brave soldiers fighting in dark basements late into the night to secure supply (Call of Duty Black Ops II).

Today: let’s include rare earths on this government critical minerals investment and state support list to show we’re serious and before we file it under nice-to-have-but-never-going-to-happen.

To use Morris’s parlance some aspects of modern life simply cannot be engineered out. And since we’re talking about the newest generation of consumer: aKsHUaLlY the kids aren’t going to harsh mining’s mellow. They’ll remain oblivious.

Nose, palate

Under Woodmac’s base case where fossil fuel demand continues to grow well into the next decade (dirty keto if you will), demand for aluminum, nickel, copper, lithium and cobalt increases at a brisk trot but it’s more or less business as usual for the mining industry.

No trillions of dollars, no inconceivably large gaps between supply and demand, just another honest day’s digging.

MINING.COM thinks Woodmac’s base case is the most likely scenario. Rather than champagne without fizz, the coming mining supercycle will be like a good Laphroig or Bruichladdich, something the analysts in Edinburgh may appreciate:

It starts gently with some soft spice, baked apples and honeysuckle, before the richness rolls in: charcoal, ash, tar, sweet-smelling leather, pungent pipe tobacco. Then things settle down and reveal a dry and ashy core with a medicinal peat and strong mineral character.

Finish

Woodmac:

“Those with a vested interest in metals are already enthusiastic cheerleaders for an intoxicating narrative about the energy transition and the quantum of metal that will be needed to achieve it.”

MINING.COM:

Get everyone another round! It’s on us!