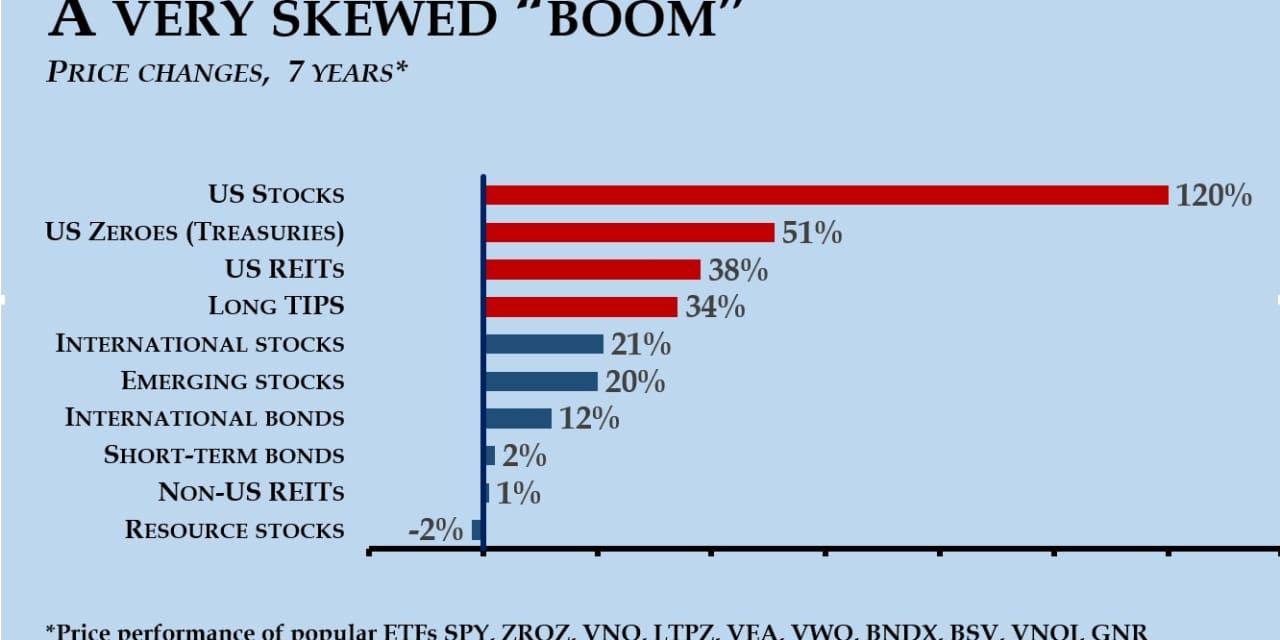

If you want to see how unbalanced markets are these days, look no further than the chart above.

It’s inspired by this column I wrote here almost exactly 7 years ago (more on this below). It covers 10 main investible asset classes that might be of interest to a private investor like you and me. And it shows the price changes since then.

Note I haven’t included in the chart the value of any dividends received. I wanted specifically to look just at price — at assets becoming more or less expensive.

The message isn’t complex. Bull market? What bull market? Over the past seven years U.S. assets, like Billy Idol, have been dancing with themselves. They’ve left everything way behind.

The chart shows the perils of portfolio allocation for those trying to save for retirement. I deliberately picked 10 asset classes seven years ago because I wanted to cover most of the waterfront of investible asset classes and outcomes. I used the phrase “perfect portfolio” but a better term would be the “No Crystal Ball Portfolio.”

“Zero coupon” or ultra-long-duration Treasury bonds, along with cash and international bonds, are insurance against a crash and deflation. TIPS, or Treasury inflation-protected securities, are protection against inflation, as are (probably) REITS and natural resource stocks. I do not, alas, have a functioning crystal ball so I have no idea what’s around the corner. Could it be a rerun of the 1930s (deflation, Depression)? Or the 1940s or 1960s and 1970s (inflation)? Or the 1980s or the 2000s (international and emerging market stocks)? Who knows?

I look at the cookie-cutter retirement portfolios that Wall Street sells to Main Street and I have to cross my fingers for America’s savers. A ‘balanced portfolio’ of stocks and bonds, totally dominated by U.S. assets? That portfolio has been terrific of late. But it’s been a flop — or worse — on multiple occasions in the last 100 years. They may not tell you that.

But seven years ago I needn’t have worried. Since then, it’s all been the USA. The “dumber” you were, the better you did. A “balanced” portfolio of 60% U.S. stocks and 40% U.S. bonds? As measured by the Vanguard Balanced Index Fund VBINX,

Someone who took a gamble and put all of their money in the S&P 500 SPX,

And someone who was even “dumber” than that, and put all their money in the 3X leveraged U.S. stock fund ProShares Ultra Pro S&P 500 UPRO,

Compared to that, a portfolio of 10 assets is trailing in the dust. Total gains, including coupons and dividends: 53%. Bah.

On the other hand, this was designed to be a low-risk portfolio that covered as many bases as possible when it came to assets and economic outcomes, not a gamble on one.

Hedge Fund Research Inc. says that its Asset-Weighted Hedge Fund Composite index (meaning the total return on all the money invested in the hedge funds it follows) has averaged 5% a year over the past five years. This portfolio over the same period: 7% a year. So let the record show just spreading your bets equally across 10 assets and then forgetting about them has been a much better investment than your typical hedge fund.

I point this out at a time when pension funds and endowments are pouring money into. hedge funds.

Spreading your bets across all these assets also seems to have held up pretty well in market crises. During the fourth quarter of 2018, for instance, this portfolio lost just 4% of its value. That’s half the loss of the balanced index fund and less than a third of the loss on an S&P 500 index fund like the SPDR S&P 500 ETF SPY,

What about looking ahead? I wonder if U.S. assets will continue to make all the running, or if the momentum will switch to overseas. The one change I’d make going forward is to replace the three stock funds. Inspired by the research of the late Robert Haugen, when I wrote the article in 2014 I targeted so-called “low volatility” stocks, which had produced higher returns over time than the rest of the market. But there is now such a factor “zoo” that I’m wary of any of them. So in watching the performance of this portfolio in the future, I’m replacing the U.S. Minimum Volatility USMV,

- iShares MSCI U.S.A. Equal Weight EUSA,

+1.49% - Vanguard FTSE Developed Markets VEA,

+1.73% - Vanguard FTSE Emerging Markets VWO,

+1.83% - SPDR S&P Global Natural Resources GNR,

+2.38% - PIMCO 25+ Year Zero Coupon U.S. Treasury Index ETF ZROZ,

-2.06% - PIMCO 15+ YEAR U.S. TIPS Index ETF LTPZ,

-0.30% - Vanguard Real Estate VNQ,

+1.64% - Vanguard Global ex-US Real Estate VNQI,

+1.41% - Vanguard Short-Term Bond BSV,

-0.07% - Vanguard Total International Bond BNDX,

-0.19%

Which of them will look terrific and which ones will be duds? Well, if we knew that ahead of time we’d all be rich.