Labor Day has been a turning point in markets the last three years. Here’s what one strategist sees happening next.

Summertime markets can be a bit dysfunctional. Last week, for example, the top two sectors were the classically defensive utilities, and the highly cyclical materials. The total market volume on the New York Stock Exchange and the Nasdaq on Tuesday was 59% below the peak of the year, and 19% below the year’s average.

Tavis McCourt, institutional equity strategist at Raymond James, points out the last two years, there was a big value and cyclical bias in stock markets after Labor Day, and in 2018, markets basically collapsed after the summer drew to a close. “We believe as the chase for the end of the year begins, a renewed value/cyclical outperformance is likely along with higher 10-year Treasury yields, but like it has been for the past 18 months and will be for the foreseeable future, the virus is the boss,” he says.

The 10-year, he says, is the linchpin to the whole market. Quantitative easing, bank liquidity, Treasury gamesmanship and delta variant fear should all fade in the second half, allowing yields to rise up to a reasonable level. That in turn will get the yield curve steepening, helping value stocks, small-caps and cyclicals — which have a long way to go, given the summer reversal in markets.

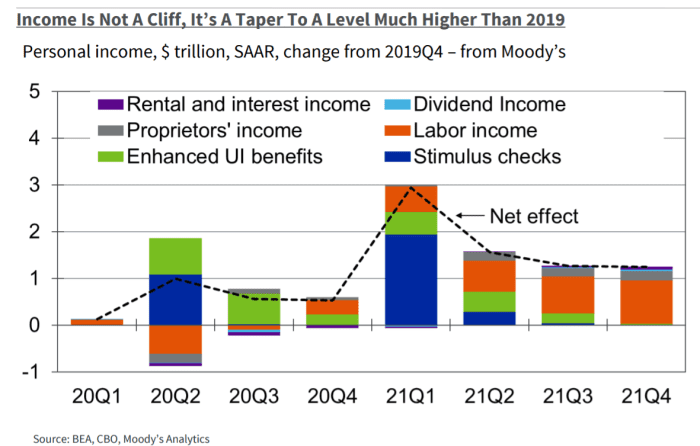

Another point he makes is there is no income or spending cliff. By the end of 2021, personal income will be about $1.2 trillion higher than the fourth quarter of 2019 — or put another way, almost exactly in line with the 4% annual average between 2010 and 2019. Since so much of the stimulus was saved, consumer spending should still grow, and an infrastructure stimulus would be a net positive.

Another huge tailwind, he says, is that financial obligations as a percent of disposable income are near 40-year lows. “Consumers have dry powder to spend, for a long, long time even with incomes returning to trend line,” says McCourt. Public company leverage also is down — on a next 12 month basis, net debt-to-Ebitda of S&P 500 companies has dropped to 1.07 in July from a peak of 1.55, and 1.28 in December 2019. Inventories, he adds, are “horribly low,” which while depressing this year’s economic output will lead to restocking demand over the next two years.

For the “de-urbanization theme,” McCourt’s stock picks are Lennar LEN,

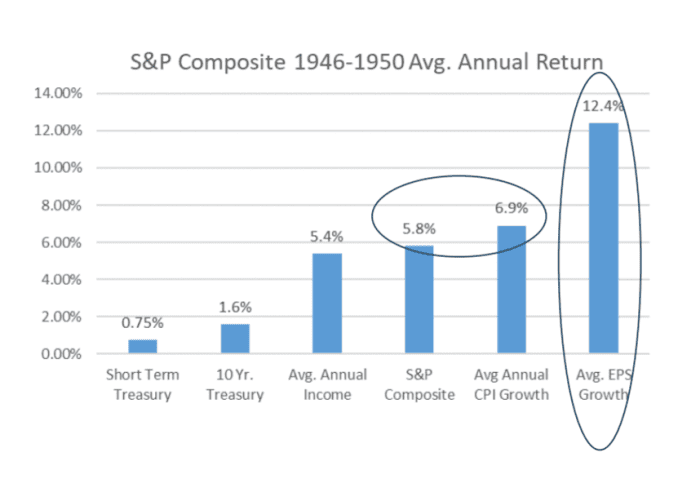

The one major risk he sees is inflation. During the late 1940s and late 1960s, short-term inflation caused 20% pullbacks, followed by inflation-adjusted returns of about zero over the next five years. In both periods, stronger than typical earnings per share growth was offset by price-to-earnings contraction, he notes.

Fed minutes on tap

Minutes from the most recent Federal Reserve interest-rate setting committee are due for release at 2 p.m. Eastern, with much of the suspense about the central bank’s direction taken away by earlier stories this week from The Wall Street Journal and Bloomberg News, that both pointed to imminent announcements that the bond-buying program will be phased out.

“In short, at this point, the Fed is just working out the details. Barring some dramatic change in the economy, tapering of asset purchases will begin in the next few months and end by the middle of next year,” said Tim Duy, chief U.S. economist at SGH Macro Advisors.

Housing starts data also are on the economics calendar.

Home-improvement chain Lowe’s LOW,

Networking giant Cisco Systems CSCO,

The markets

Stock futures ES00,

The tweet

Ajmal Ahmady, until Saturday the central bank chief of Afghanistan, gave a pretty grim diagnosis for the economy.

Random reads

This hacker stole $610 million — and got a job offer from the victim.

Hobbits were a real thing, fossils suggest.

Need to Know starts early and is updated until the opening bell, but sign up here to get it delivered once to your email box. The emailed version will be sent out at about 7:30 a.m. Eastern.

Want more for the day ahead? Sign up for The Barron’s Daily, a morning briefing for investors, including exclusive commentary from Barron’s and MarketWatch writers.