(Bloomberg) — The twin issues that have recently rocked stocks — the omicron coronavirus variant and a hawkish Federal Reserve — did nothing this week to deter dip buyers, who powered American equities to their best rally in 10 months.

Most Read from Bloomberg

As the latest Covid-19 strain sparked fresh restrictions around the world and surging consumer prices kept the Fed on track to tighten, bargain hunters poured back in, powering the S&P 500 to an all-time high with gains in four of the five days. Hedge funds, who cut equity exposure at a ferocious pace during the November rout, re-emerged as buyers. Equity funds lured money for an 11th straight week. And bullishness crept higher in the options market.

It’s another lesson for bears that’s been driven home repeatedly in 2021: betting against stocks has become futile. Dip buyers have been rewarded virtually every time the market has pulled back, so much so that by one measure the strategy is having one of its best years on record.

“All of our fears seem to have been overblown about 2021, and that’s proved to be a successful environment for dip buyers,” said Art Hogan, chief markets strategist at National Securities. “Nothing succeeds like success, and when that pattern starts to repeat itself, it gets noticed and more people join the game.”

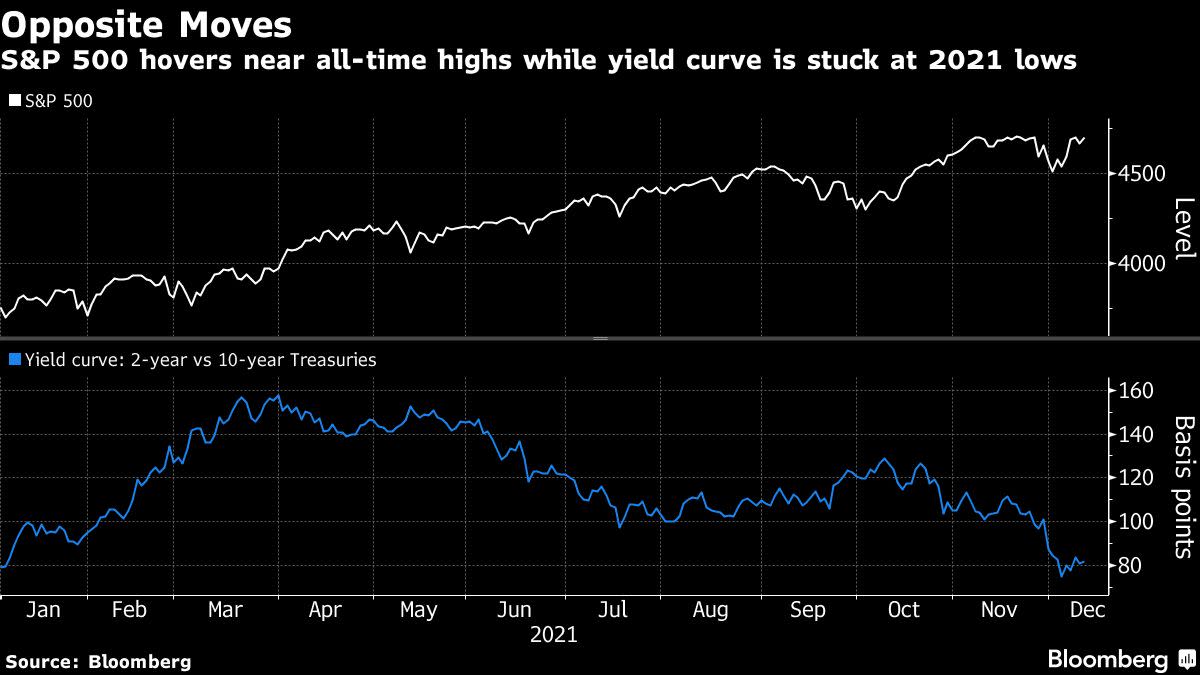

The latest episode has bulls basically ignoring an ominous sign from the bond market, where short-term rates are rising, while long-term ones fall. This flattening of the yield curve is viewed by many as a message that the Fed is poised to snuff out the economic growth that’s been rocket fuel for corporate earnings.

Stock buyers argue that a booming economy can withstand the anticipated two 25 basis-point rate hikes next year after the Fed signaled it would move faster to wind down its bond-buying program. And even though data Friday showed consumer prices rose the most in four decades last month, views on the pace of tightening did not get more dire.

“By speeding up taper and starting rate hikes early, the Fed should be able to proceed at a pace that doesn’t threaten the expansion,” said Steve Chiavarone, portfolio manager and head of multi-asset solutions at Federated Hermes. “So you’ll see the 10-year go up more as the market gets comfort that the growth they’re seeing today will persist for some time.”

The equity faithful can be forgiven for focusing on the bright side because every threat in 2021 — from supply-chain disruptions to commodity inflation to the new coronavirus variant — has done nothing to halt the $30 trillion rally since the pandemic trough in March 2020.

After two weeks of declines, the S&P 500 started this one with the best three-day rally in more than a year. Traders went risk-off Thursday ahead of the widely followed inflation data, only to return the next session and power the S&P 500 to its first record in almost a month. All told, the benchmark index climbed almost 4% for the best week since February.

The dip-buying strategy has rewarded investors throughout the year after big down days. Since January, the index has posted 19 sessions of dropping more than 1%. Thirteen of them were immediately followed by an up day. The 68% win rate is poised to be the third-best for any year since 2007.

Hedge funds, who slashed their equity exposure at the fastest pace since April 2020 during the prior two weeks, were back as a source of demand. They were net buyers of stocks for the first time in four weeks, driven mostly by a reduction in bearish positions, according to data compiled by Goldman Sachs Group Inc.’s prime brokerage.

More broadly, investors keep pouring money into stocks. Funds focused on U.S. equities attracted $8 billion of fresh money over the week through Wednesday, Bank of America Corp. said, citing data from EPFR Global.

In the options market, bears retreated, with the Cboe equity put-call ratio falling from a 13-month high. Apple Inc., which climbed almost 11% this week, saw bulls snapping up call contracts to wager on further gains.

“Fear of missing out is still alive,” said Alon Rosin, Oppenheimer & Co.’s head of institutional equity derivatives. Though he noted some nervousness among money managers who are under pressure to preserve performance heading into year-end while the Fed’s policy meeting looms next week. There are “lots of cross currents clearly with the biggest mystery being how will this market really digest the Fed’s ‘new stance’ ahead,” he added.

Rate anxiety was evident underneath the surface of market buoyancy. From initial public offerings and shares of unprofitable technology companies, the speculative corners of the market have yet to recover their post-omicron declines despite the recent gains. In fact, year-to-date, they’ve suffered deep losses, in stark contrast with the S&P 500 that’s up more than 20%.

The carnage in IPOs and risky tech names reflects a valuation threat from higher interest rates, according to Jason Thomas, head of global research at Carlyle, a private-equity giant.

“There’s going to be much stricter scrutiny for when they are going to ever be profitable,” Thomas said. “The successes are going to be held longer because they have to grow into the new valuations.”

To Sarah Hunt, a portfolio manager for Alpine Woods Capital Investors, while any Covid-induced dip is worth buying — the economy will eventually open, investors had better heed the moves in the bond market.

“The flatter curve suggests that the long-term growth story is fragile,” she said. “You are seeing weakness in some of the higher flying valuation areas, and I think with rates poised to move higher, that continues. Maybe valuations will matter again, we can only hope.”

Most Read from Bloomberg Businessweek

©2021 Bloomberg L.P.