Fitch forecasts the growth in global lithium mine production to accelerate in the coming years, as existing new projects make quick progress while new projects emerge amid the strong momentum behind the green transition and batteries.

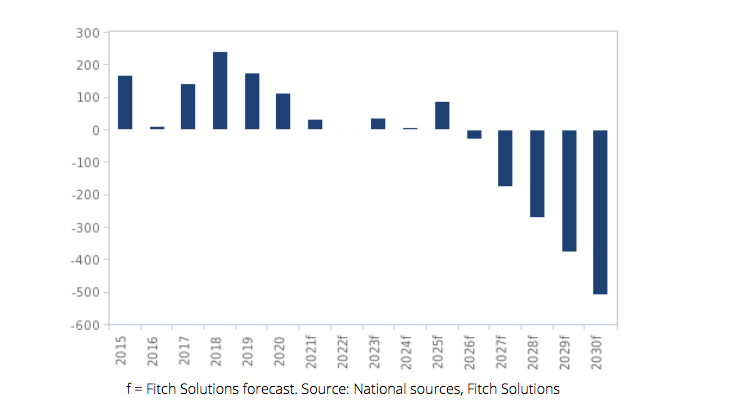

The analyst’s country-by-country forecast shows expected global output to rise by about 600,000 tonnes lithium LCE between 2025 and 2021 (compared with the 2021 production), compared with the 240,000 tonnes added between 2016 and 2020. Fitch also sees production rising by 290,000 tonnes between 2026 and 2030 — with that long-term estimate on the conservative side.

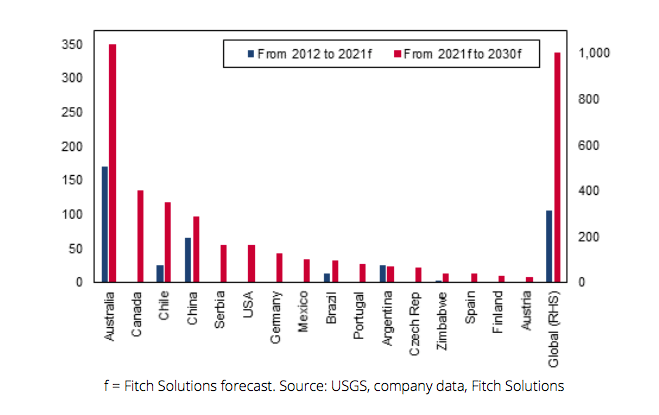

Well-established lithium-producing countries will record further growth, Fitch says, while a number of new lithium- producing markets will emerge in the next 10 years. Fitch sees production growth accelerating in Australia, where output in the country is set to almost triple over 2020-2030. Chile and China will also more than double their output, while we see production in Brazil will grow five-fold (from a lower base). Although Argentina will also record significant growth, output will ‘only’ double.

Amid rising interest, government support and increasing capital dedicated towards lithium projects, a notable number of new lithium-producing countries will emerge and altogether account for a significant share of global output by 2030, the analyst says. These include mostly developed markets (DMs) such as the US, Canada, Germany and some other European countries, along with developing countries such as Mexico, Serbia and Zimbabwe (although the country does produce some non-battery grade lithium currently), Fitch notes.

Lithium can be extracted via several very different techniques, and new and potentially more environmentally friendly extraction techniques are emerging at different stages of development.

In any case, they suggest that actual supply could rise faster expected. Currently, only hard rock (‘traditional’ mines, located, for example, in Australia, Brazil, China and Canada) and ‘conventional’ brine resources (from salars, located, for example, in Chile and Argentina) are used to produce lithium chemical products commercially at a large scale.

However, a host of new players are developing new extraction techniques, namely geothermal brines and sedimentary (clay) deposits, which could upend primary supply of lithium, says Fitch.

As these new extraction techniques make progress, the structure of the industry, shape of the cost curves and ESG considerations will continue to evolve, the analyst notes. The upcoming development of lithium recycling could also ease some of the lithium supply issues in the longer term.

Lithium supply will face a number of vulnerabilities, including geographical concentration at both the mining and refining level, as well as the limited presence of established and large mining players, which pose risks to the project pipeline execution, Fitch says.

Rising resource nationalism in key lithium markets could also hamper the development of new projects.

However, Fitch notes that lithium reserves are ample and keep on growing, suggesting plenty of potential to boost supply in the long term.

(Read the full report here)