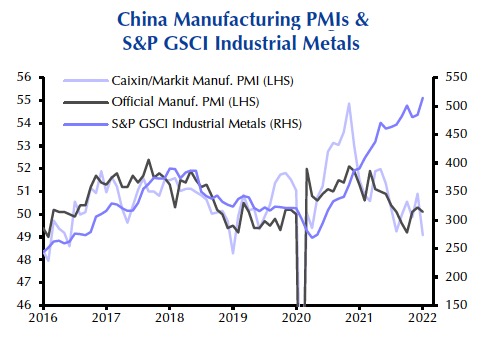

A reading of the official Chinese manufacturing purchasing managers’ indexes (PMIs) for January shows activity falling again from the previous month and at 50.1 is now approaching contraction territory.

A PMI reading over 50, or 50%, indicates growth or expansion of the manufacturing sector as compared with the previous month, while a reading under 50 suggests contraction.

The Caixin gauge, which gives better insight into smaller and medium-sized businesses compared to the official count which gives more weight to large state owned enterprises, plunged from 50.9 in December to 49.1. An average of the two PMIs shows weakness in manufacturing not seen since February 2020.

Capital Economics says Chinese demand should result in markedly lower industrial metals prices as energy supply shortages ease later this year, although there are risks to this scenario:

There are already signs that this process is underway; our estimates show that China’s stocks of crude oil ticked up in December, and stocks of coal at Chinese power plants are now in a much healthier position than they were a few months ago.

Nevertheless, there remain several risks that could derail the recovery in energy supply (and consequently keep industrial metals prices elevated). Most notably, much will depend on how the ongoing Russia-Ukraine tensions pan out, and to what extent this results in lower energy supply from Russia.