We’re well into earnings season, and so far, investors should be gratified by the results. Cumulatively, some 56% of the S&P 500 companies have reported so far; of those, 79% have beaten earnings estimates. Overall, earnings are up 45% in the past 12 months, and this is the fourth quarter in a row with sequential gains of 25% or more.

While the earnings season has been solid, there is one cautionary note – the immediate comparison is to 2020, when the COVID pandemic had a negative impact on a wide swath of sectors and pushed down earnings. Still, the rebound is significant, and indicates underlying economic strength.

With this in mind, we used TipRanks’ Earnings Calendar to get the lowdown on 3 Strong Buy tickers reporting quarterly results later this week. Let’s dive in and see what makes these stocks stand out.

Enphase Energy (ENPH)

We’ll start our look with Enphase Energy, which reports its 4Q21 earnings on February 8 after the markets close. Enphase is a designer and manufacturer of solar inverters, an essential hardware technology in solar power industry. Photovoltaic solar panels produce direct current (DC) electricity, which inverters convert to the alternating current (AC) power that is transported by the electric grip and used in our applications. Enphase was the first company to offer commercial-scale inverters on the market, and remains a leader in the solar power industry.

Heading into the Q4 results, a look back at Q3 can provide some insight. Enphase reported $351.5 million at the top line, a company record, and 60 cents per share earnings, the highest in over two years.

Looking ahead to the Q4 results, Enphase has high hopes. During the fourth quarter, Enphase launched its latest product, the IQ8 microinverter. This is billed as the most advanced such device on the market today, and is considered a ‘smart’ device, able to form its own microgrid to supply power during an outage – directly from solar energy. The IQ8 does not require a battery system during daylight. The higher price of the IQ8 device, compared to its predecessors, should offset increases in materials and manufacturing costs.

Nothing exists in a vacuum, and Enphase faces regulatory and policy issues that are unique to the solar industry. The Biden Administration’s failed Build Back Better bill included a strong push to solar power, that would have been a boon for Enphase; the company now must be patient and see if any of those provisions are enacted independently by Congress. And, in California, the state government attempted to push a power utility regulation that would have seriously constrained the residential solar market. Popular pushback is forcing the state authorities to reconsider.

The likelihood of an improved regulatory environment has Guggenheim analyst Joseph Osha somewhat bullish. He writes of Enphase’s near-term prospects, “We think that valuations and investor expectations have become more reasonable. At the time we cut our ratings in October, the majority of our estimates for 2022 were below consensus. That is no longer the case, and we believe that investors can start 2022 with some confidence that they aren’t looking at downward revisions… It is important to remember that even in a scenario where California policy takes a sharp turn for the worse, the market transition mechanism could actually drive better demand for the near term…”

Osha, a 5-star analyst, puts a Buy rating on Enphase, along with a $213 price target that suggests an upside of ~49% in the year ahead. (To watch Osha’s track record, click here)

The Street’s outlook on Enphase remains bullish, with the 18 recent reviews including 16 Buys and 2 Holds, for a Strong Buy consensus rating. The shares are selling for $142.04 and the $234.94 average price target implies a one-year upside potential of ~65%. (See ENPH stock forecast on TipRanks)

Mattel, Inc. (MAT)

Some companies need no introduction. Mattel, with its familiar red logo and a product line that includes Fisher-Price, Barbie, and Hot Wheels, is one of those. Most of us grew up with Mattel products, or are getting them for our kids, and brand loyalty has long been a source of support for the company, which is the world’s fourth-largest toy maker by total revenue.

In January of this year, Mattel scored an industry win, when it regained the rights to produce toys under the Disney franchise. The company has lost this franchise to rival Hasbro in 2016; regaining it was seen as a major coup. In 2016, the Disney franchise was worth over $440 million for Mattel. The company expects similar results going forward with Disney-branded products, which are expected to hit the shelves under Mattel’s logo in 2023.

Mattel shows a strongly seasonal pattern to its quarterly revenues and earnings, with the highest results in Q3 and Q4; the first half of the year typically shows about the half the revenue of 2H. Looking back, Mattel had $1.76 billion in its 3Q21, up 8% year-over-year. The company’s Q4 results typically repeat those from Q3, on holiday season purchases. Mattel will release its 4Q21 results on February 9, after the markets close.

Covering Mattel for MKM Partners, analyst Eric Handler writes: “We look for continued positive momentum from Mattel’s product portfolio in 2022 and believe guidance for MSD net sales growth (in constant currency) will prove conservative as could its $1bn+ adjusted EBITDA projection… Based on our positive view towards Mattel’s movie license tie-ins, further progress with its turnaround brands, and its relaunched brand efforts, we project net sales of $5.60bn (+5%), a level which we believe has upside potential and is above consensus of $5.5bn.”

To this end, Handler gives Mattel a Buy rating, and his $30 price target indicates his confidence in an upside of ~39% over the next 12 months. (To watch Handler’s track record, click here)

Overall, the 5 recent reviews on Mattel stock include 4 Buys against just a single Hold, supporting a Strong Buy consensus view. The average price target, at $31.75, is somewhat more bullish than Handler allows, and implies potential share appreciation of ~47% this year. (See MAT stock forecast on TipRanks)

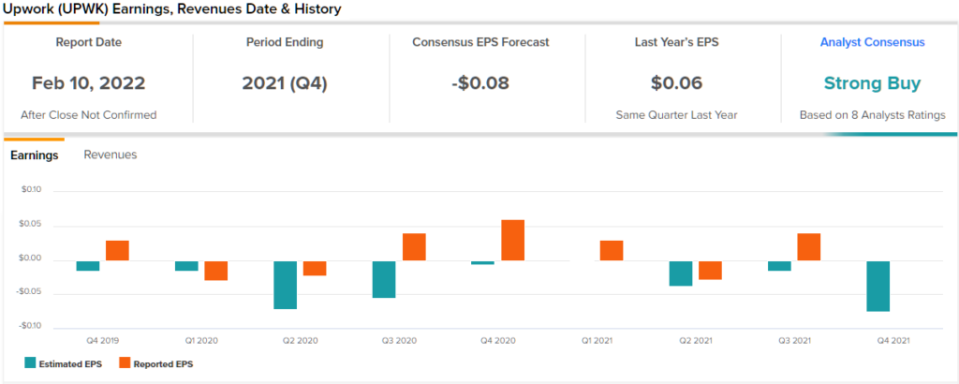

Upwork, Inc. (UPWK)

Last but not least is Upwork, the online freelance marketplace. Upwork was formed in 2015 through the merger of Elance and oDesk, and went public in October 2018. The stock saw a surge in value in November 2020, in line with the ‘push’ online business got from the COVID crisis. Even without that, however, Upwork has been on an upward trend; the company has seen revenue increase sequentially in every quarter for the past two years.

The company’s Q3 earnings disappointed investors, however, and the stock has been falling since the October 27 release. While revenues were up 33% year-over-year, EPS came in at a 4 cent per share loss where the forecasts had predicted a 1-cent EPS profit. Looking ahead, revenue for the fourth quarter is expected to be $130 million to $132 million, up only slightly sequentially, and non-GAAP loss is expected to be $0.03 to $0.05 per share.

BTIG analyst Marvin Fong sees plenty of positives ahead of the company’s Q4 earnings release on February 10 after the markets close. He explains: “The tight labor market (unemployment at <4%), the spread of the Omicron variant and wage inflation could be prompting employers to turn to freelancing. We also like that UPWK is B2B and service-focused, which should help UPWK avoid pressures from consumers returning to some of their pre-COVID retail purchasing behavior, a dynamic that has waylaid some other e-commerce companies. Additionally, we see UPWK as benefiting from inflation as companies look to manage labor costs.”

In line with these comments, Fong puts a Buy rating on Upwork stock. His $50 price target is bullish, and suggests the stock has ~82% upside ahead of it. All of this makes Upwork one of Fong’s ‘Top Picks.’ (To watch Fong’s track record, click here)

Wall Street is generally taking an upbeat stance on Upwork, giving the stock a Strong Buy consensus with 7 Buys out of 8 recent reviews. UPWK shares are trading at $27.49 with a $46.13 average target; this gives the stock an upside of ~68% in 2022. (See Upwork stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.