Inflation and the Federal Reserve’s potential reaction to it have the stock market all shook up.

But like early concerns that Elvis Presley and rock ‘n’ roll would ruin the country, these are just false fears. So stocks are a buy every time the market hits replay on this song.

Thursday’s decline in the stock market won’t be the last. Inflation, which the government reported came in at a searing 7.5% for January, will print high for a month or two. But inflation will show signs of calming down this summer and throughout the second half of the year.

This will ease fears of a 1970s-style wage-price spiral that would have the Fed doing a Paul Volcker 2.0 hatchet job on growth. To fight inflation, Fed chair Volcker hiked rates so much in the late 1970s and early 1980s that he slammed the economy into a painful recession.

That’s not going to happen this time around, for the reasons below. Growth will continue to be OK because of embedded forms of stimulus, including: Low inventories that have to be rebuilt; strong consumer and corporate balance sheets; and low consumer confidence, which has plenty of room to improve as the Covid decline becomes more evident.

“If we see inflation coming down on its own, that would bring great joy and cheer to the markets,” says Ed Yardeni, of Yardeni Research. “That would mean the Fed doesn’t have to catch up in an abrupt fashion.”

That’s Yardeni’s take, and I think he’s right for the following five reasons.

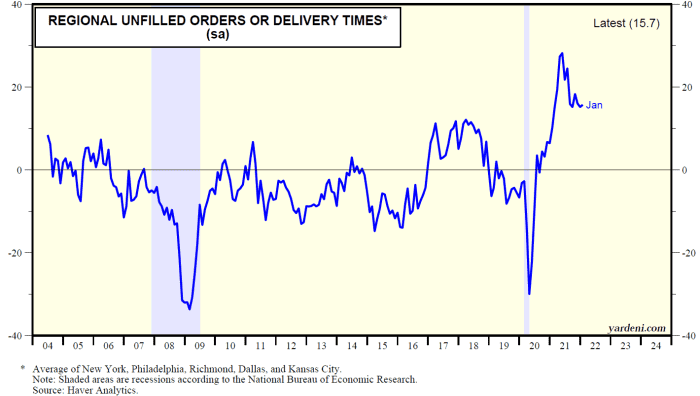

Reason #1: Supply-chain issues are a fixable problem

Covid really screwed up supply chains, as lockdowns and worker illnesses got in the way. This created shortages, which drove up prices. But with Omicron shifting Covid into an endemic phase, supply chains are getting fixed. The related pricing pressure will ease.

For example, one of the big drivers of inflation is the rise in auto prices, thanks to chip shortages limiting production. But Japan’s auto production rose in November and December, according to Haver Analytics. If Japanese companies can find chips, then others will too. Improved production will bring down soaring used and new car prices, predicts Yardeni.

We see signs that supply chains are already being repaired, as there’s been a decline in unfilled orders.

Reason #2: Demand shock is waning

Besides Covid, a demand shock crippled supply chains. When governments and central banks throw tons of money into the economy, guess what? People spend it freely. That drives up prices.

Now, though, the free money is dwindling. Generous unemployment benefits have ended. President Joe Biden’s failure to get Build Back Better passed signaled the end of trillion-dollar Covid-era spending plans.

“We won’t get any more fiscal stimulus, so demand will simmer down,” says Yardeni.

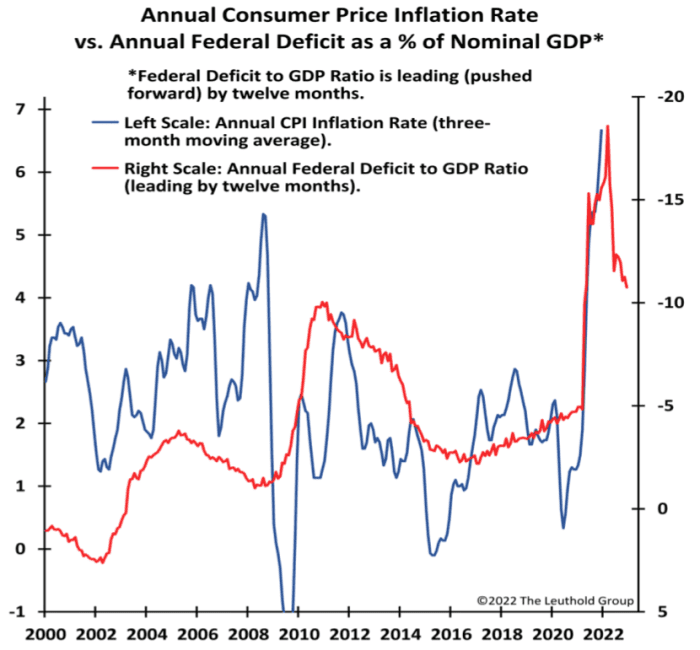

The Fed will soon start trimming its balance sheet. This will ease demand pressures, too.

In the chart below, we see that the contraction in the federal deficit relative to GDP can foreshadow a decline in inflation. The chart comes from James Paulsen, an economist and chief market strategist at the independent research firm Leuthold. Note that the red line representing the deficit-to-GDP ratio is pushed forward by a year, because of the lag in the impact this has on inflation.

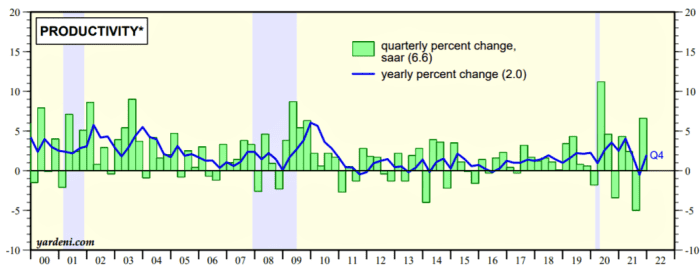

Reason #3: Productivity is coming to the rescue

Thanks to labor shortages, companies have really increased their spending on technology and machines (capital spending) to boost productivity. Defined as output per worker, productivity goes up when the technology-to-labor ratio increases in the workplace.

You can see this in the big increase in durable goods orders, but companies are telling us the same thing. Blackstone BX,

As companies get more output from the same labor cost, they feel less pressure to pass their own cost increases on to customers. That is happening now. We know this because profit margins are holding up despite labor cost increases.

The chart below also confirms that productivity, while volatile, is consistently higher since the start of the pandemic. In contrast, during the 1970s wage-price spiral, productivity growth had collapsed — one reason the Fed had to play rough.

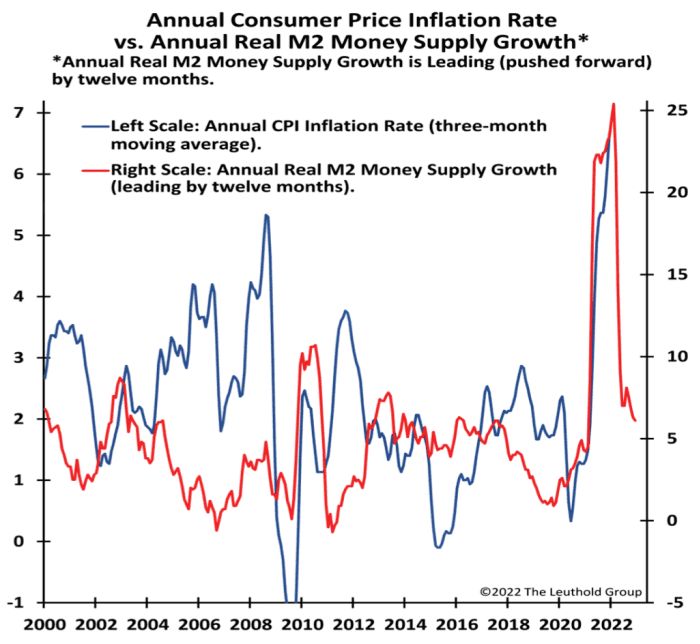

Reason #4: Money supply growth is slowing

This is a pretty good predictor of inflation, says Paulsen. This makes sense, because when people get more money (more is injected into the economy), they tend to spend more, driving up prices. Currently, money supply growth is contracting, so inflation will too.

In the chart below, the red line representing money supply is pushed forward by one year. That’s because the change in money supply growth affects inflation with about a one-year lag.

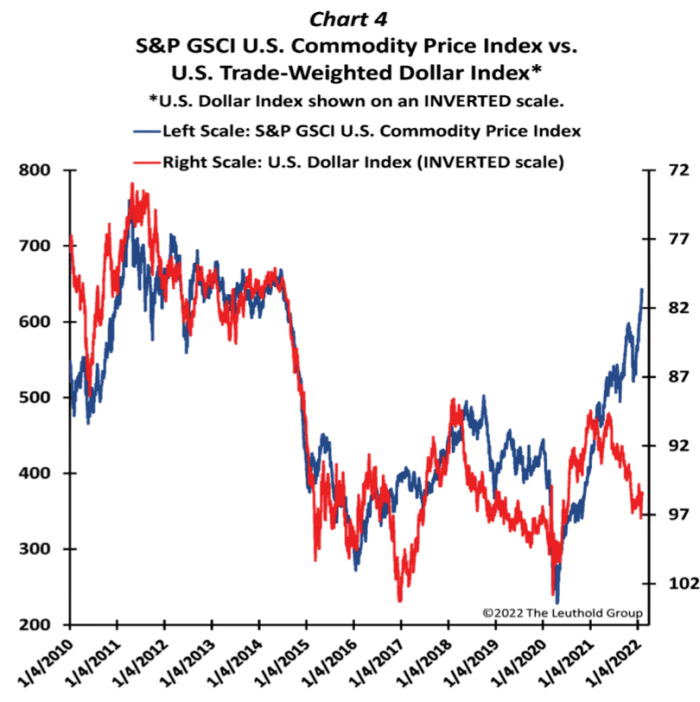

Reason #5: The dollar is strong

A strong dollar reduces foreign demand for U.S. products. This cools off inflation in the U.S. That is happening now. This chart shows the tight relationship between the dollar and U.S. prices. The red line representing the dollar is on an inverted scale, which means it declines as the dollar strengthens. The blue line is prices.

It’s a good time to buy stocks

All of this tells us that you need to buy whenever your fellow investors freak out and sell stocks because of fresh worries about inflation forcing the Fed to play tough. That’s not going to happen because inflation will subside.

The inflation and Fed panic this week won’t be the last, since signs of inflation’s decline probably won’t appear until April or May. Plus, the Fed still has to start hiking rates and trimming its balance sheet. These moves could cause tremors, too.

Yardeni thinks the S&P 500 SPX,

“We would use the cash to buy stocks on dips,” he says.

Companies have so much cash ($3.7 trillion, excluding holdings of equities and mutual funds), they may be right there with you, buying the pullbacks. Or buying other companies in the weakness, as we saw in January. Purchases of companies in tech in January were the second-highest on record.

The “Fed put” may be kaput, but the “CFO put” may replace it, says Yardeni. He favors energy, financials and beaten-down tech.

If, like me, you favor stocks that insiders are buying, here are three to consider in these sectors.

Continental Resources

I was singling out Continental Resources CLR,

Western Alliance Bancorp

Bank stocks have been strong. But Western Alliance Bancorp WAL,

Microsoft

Like most tech companies, Microsoft MSFT,

One big challenge remaining?

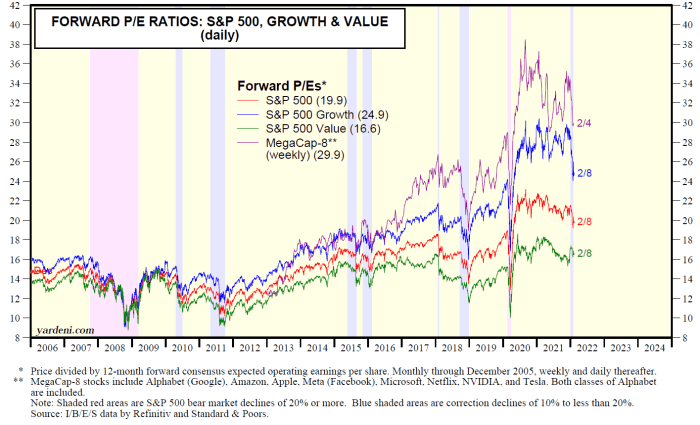

One problem for stocks right now is that inflation tends to weigh on valuation multiples. But this may have already played out. It sure looks like it, in the chart below. Should inflation begin to ease, so will these valuation contractions.

Michael Brush is a columnist for MarketWatch. At the time of publication, he owned MSFT. Brush has suggested CLR and MSFT in his stock newsletter, Brush Up on Stocks. Follow him on Twitter @mbrushstocks.