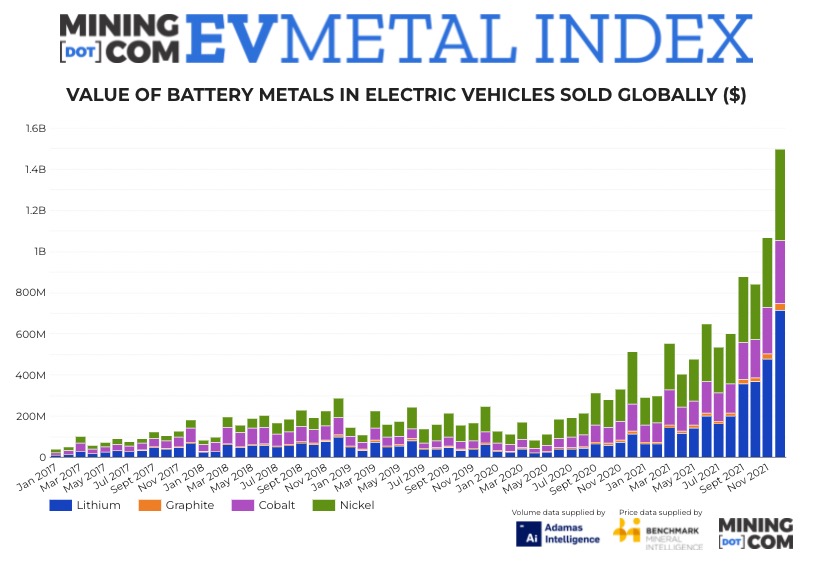

Total battery capacity of the 1.25m EVs sold during December set a new monthly record, surging 71% year on year to 43 GWh according to Adamas Intelligence, which tracks demand for EV batteries by chemistry, cell supplier and capacity in over 100 countries.

Annual EV sales in 2021 surged to over 10m, with full battery electric vehicles responsible for 46% and plug-in hybrids 19% of the total.

In order to produce the most accurate data, the monthly battery capacity deployed numbers in the MINING.COM EV Metal Index do not include cars leaving assembly lines, those on dealership lots or in the wholesale supply chain, only end-user registered vehicles.

As such, the tonnages reflected in the end-product are fractions of what would have been procured from mines, with losses in yield during chemical conversion, and cell, cathode and battery manufacture.

Lithium

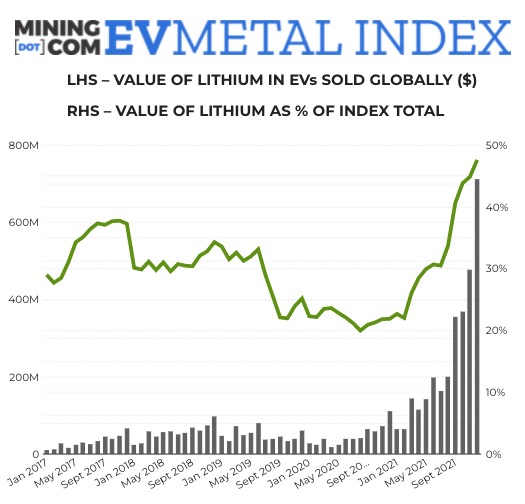

In December 2021, a record 25.9 kilotonnes of lithium carbonate equivalent were deployed onto roads globally in batteries of all newly-sold passenger EVs, 68% more than in the previous year and a 31% increase over November according to Adamas.

Average lithium on a per vehicle basis (including hybrids) was up 12% year over year in December, jumping from 18.5kg to 20.7kg, a testament to the relative popularity of full electric cars over hybrids.

Carbonate made up 57% of the total as demand for nickel and cobalt-free LFP batteries continues to strengthen versus hydroxide’s 43%, with the latter favoured in the manufacture of high-nickel content batteries.

Lithium prices have jumped across the board over the past year, but inside China there is a mad scramble, particularly for carbonate, which continues to soar in 2022 after more than quadrupling in value last year according to Benchmark Mineral Intelligence, a battery supply chain researcher and price reporting agency.

A massive gap has opened up between ex-works prices in China for minimum 99.5% battery grade carbonate which is now trading in the $60,000 a tonne range according to Benchmark’s mid-February price update with scarcity exacerbated by maintenance downtime at chemical plants during Chinese New Year.

That compares to European prices for carbonate of $30,000 (CIF minimum 99%, Jan 2022). Benchmark also points out that the premium of lithium carbonate over lithium hydroxide – used in high nickel cathodes – reached nearly $20,600/tonne in February. Historically hydroxide has always been the pricier one.

Benchmark in a recent report said record high Chinese lithium carbonate prices have pushed the costs of LFP cells at least 5% higher than high-nickel cells on a dollar per kilowatt-hour basis, in a reversal of a decade-long trend.

“The turnaround highlights the acute pricing pressures facing producers of LFP battery cells in China, which could translate into higher prices for electric vehicles and energy storage systems.”

The lithium subindex topped $700 million for the first time in December. As a percentage of the overall index value, lithium now has the biggest share, surpassing that of nickel. From a low of 20% in 2020, when prices spent several months under $7,000 a tonne, to just over 47% now.

Cobalt

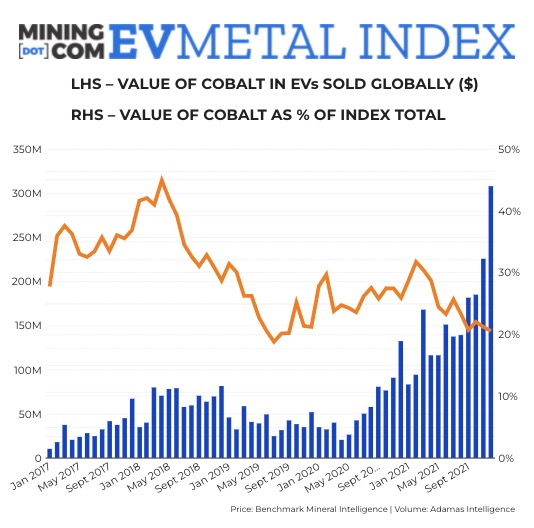

At over 4,000 tonnes for the first time, cobalt deployment rose 36% in December, compared to the same month last year and recorded a 25% month on month jump. On a per vehicle basis cobalt use dropped 10% from last year, another indication of the popularity of LFP-equipped vehicles and the move to lower cobalt cathode chemistries for NCM batteries.

Cobalt hydroxide used in the battery supply chain has surged over the past year topping $65,000 a tonne (100% Co basis) in January, the highest price since June 2018. Chinese factory cobalt sulphate prices are up 57% over the past year while battery metals prices are up 93% to over $34 a pound.

Despite the price appreciation, cobalt’s share of the EV Metal Index continues to shrink, reaching 20.6% in December. That compares to 45% in April 2018 when the metal was on its way to record highs.

Nickel

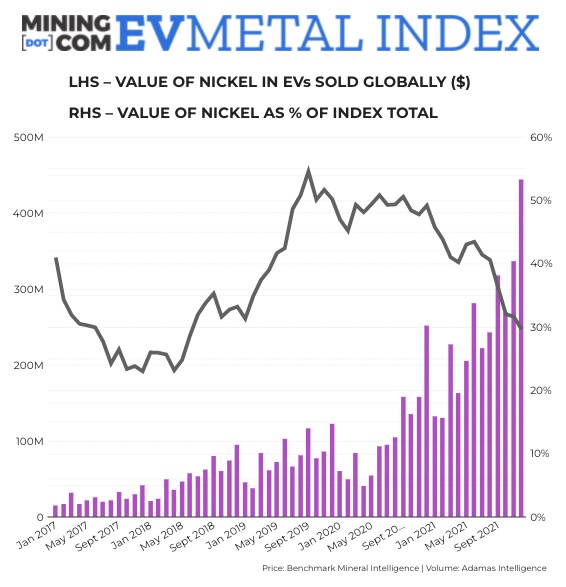

Nickel use was up 44% compared to the same month last year with a new record during the month of 19.6 kilotonnes while on a per vehicle basis nickel use declined 4% to 15.7kg. Nickel sulphate climbed to $22,600 a tonne (100% Ni basis) level in December according to Benchmark data, but premiums over nickel metal traded on the LME continued to shrink.

Nickel hit a decade high above $25,000 a tonne on Monday on worries that Ukraine tensions could disrupt supplies from Russia at a time of dwindling global inventories of the metal and a spot market in backwardation when prompt delivery contracts are priced higher than futures.

Graphite

In December 2021, just shy of 39 kilotonnes of synthetic and natural graphite were deployed globally in batteries of all newly-sold passenger EVs, also a record tally. The monthly total represents 78% jump over the same month last year.

On a per-vehicle basis graphite use is up 19% year on year to 31kg when taking into account full battery, plug-in hybrid and conventional hybrid vehicles.

Graphite prices have increased more than 20% since December 2020 at roughly $860 a tonne according to Benchmark data, after spending all of 2020 below $700 and hitting a low of $644 in September. Prices for the anode material peaked above $1,500 a tonne in early 2012.

")