Don’t miss CoinDesk’s Consensus 2022, the must-attend crypto & blockchain festival experience of the year in Austin, TX this June 9-12.

Google (or DDG) “inflation” and you’ll find articles with headlines from basically every media outlet saying something like: “US Inflation Jumps to Fresh 4-Decade High of 8.5% in March.” That’s a big number. When inflation fear enters the conversation, investors go “risk-off,” and they pile into inflation hedges and store-of-value assets like gold and … like bitcoin?

Well then, why didn’t bitcoin’s price rocket up after the inflation print came out last week? Is bitcoin a bad inflation hedge? Is it ever going to be a store of value? For all its promise, Bitcoin’s sound money properties should predispose it toward being a useful inflation hedge and store of value. That has fallen flat. So what gives? How aspirational is the “bitcoin as a store-of-value” narrative? Are bitcoin investors screwed? Why is bitcoin acting like a tech stock?

That (and maybe more) below…

– George Kaloudis

You’re reading Crypto Long & Short, our weekly newsletter featuring insights, news and analysis for the professional investor. Sign up here to get it in your inbox every Sunday.

Prevailing economic theory is built upon three pillars: output, money and expectations. The people and groups that run economies want to increase economic output and strengthen their sovereign money against other currencies while managing expectations for the future to avoid economic downturns. There’s not enough room in a column to dive into the gory details of all of these concepts, but let’s zoom in on money, expectations and the entity responsible for those two in the U.S., the Federal Reserve, and tie it into recent inflation woes (and Bitcoin!).

The Fed has been given responsibility for monetary policy in the U.S. and aims to ensure “maximum employment, stable prices and moderate long-term interest rates.” The Fed has three levers it can pull to achieve its goal: 1) open market operations (i.e. “print money”), 2) the discount rate (i.e. “interest rates”) and 3) reserve requirements (i.e. “vault deposit rules”). Printing money (by buying bonds and “stuff”) and changing interest rates (by changing the rate it charges banks to lend money overnight) are the main mechanisms we’ve seen the Fed employ in recent memory.

And, wow, does the Fed have its hands full right now.

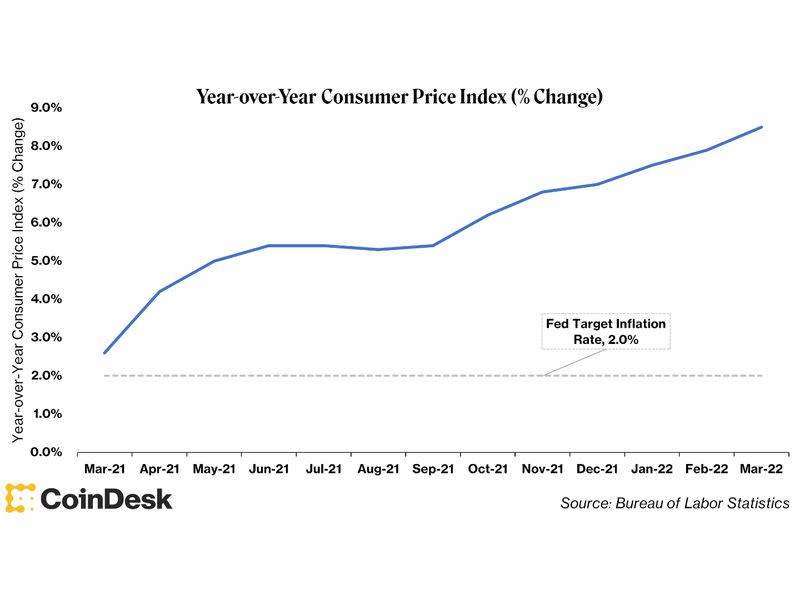

“Stable prices” is a goal for the Fed, and that has historically meant an arbitrary 2% target for inflation each year, meaning the Fed wants things to cost 2% more each year. Well, last week the consumer price index, a means to measure inflation, jumped to a four-decade high of 8.5% year-over-year in March. Basically, last year’s $10 burrito is now $10.85. That is not a good thing. On top of that, year-over-year CPI metrics have exceeded 2% every month since March 2021. Inflation is clearly not transitory.

I’m not going to talk about how unprecedented money printing and near-zero interest rates might have led us here. Instead, I’m going to talk about what investors are doing to protect their portfolios.

In times of high inflation and economic uncertainty, investors go risk-off, and there’s a “flight to quality.” In practice, when sentiment flips risk-off, investors sell their risky tech stocks and buy something like bonds, or if they really fear inflation, something sound like gold.

And you know what’s better than gold? Gold 2.0 of course. Bitcoin (or the Reserve Asset 3.0). We have high inflation, and so everyone piled into bitcoin and its price shot up, right? Not quite…

What gives? This is sound money, right? This is a store of value with a known current supply and emissions schedule, right? Isn’t bitcoin provably scarce? I thought the emissions schedule of bitcoin didn’t change as demand for the asset increased?

That’s all true: Bitcoin has a known monetary policy with a hard cap and a predetermined minting schedule; anyone with a full node (a basic computer with some software) can tell you how many bitcoins are in circulation and if the price of bitcoin went to $1 million tomorrow, the coins wouldn’t be mined any faster than they are today.

But there’s one thing missing.

Narrative.

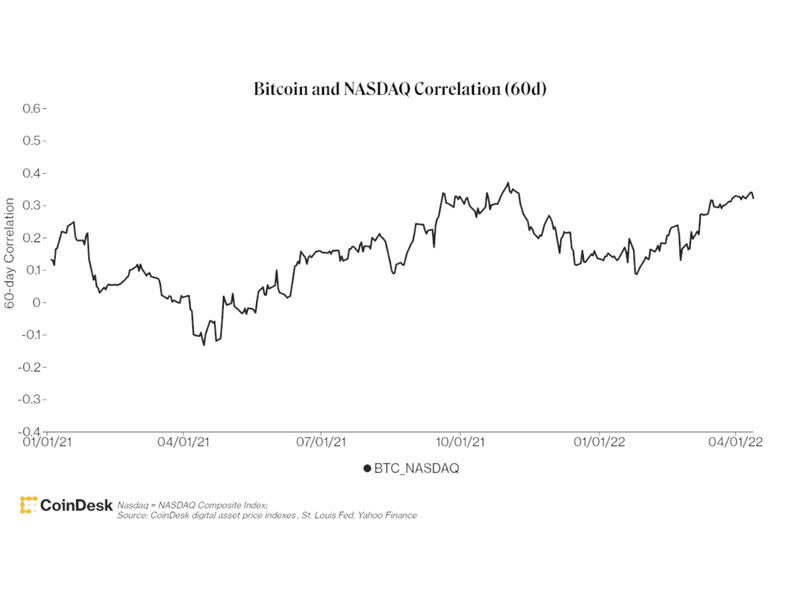

On a 60-day lookback, bitcoin’s price has been somewhat correlated (> 0.20 correlation coefficient) with the technology stocks in the Nasdaq for about 50% of trading days in 2022. I think the reason for that is quite simple. While bitcoin’s hard money properties make it a risk-off asset for its supporters, investors see a risk-on asset because of its volatility and technology-like asymmetric price upside. When investors want to cut risk, they sell stocks alongside bitcoin. So bitcoin isn’t a risk-off or risk-on asset yet. Instead, I think it’s better to call it “risk everything.”

As such, it is probably more accurate to refer to bitcoin as an aspirational store of value. Yes, a borderless, permissionless, uncensorable, sound monetary system-of-value transfer with a predictable monetary policy is theoretically a great store of value, but until that narrative penetrates more than 100 million people, the other 7.8 billion people won’t view that system as a store of value, and that narrative will prevail. For now.