How high can the Fed hike interest rates before a recession hits? This chart suggests a low threshold.

The days when the Federal Reserve could raise its benchmark interest rate significantly above 5% without sparking a recession may be a thing of the past, according to Wells Fargo Investment Institute.

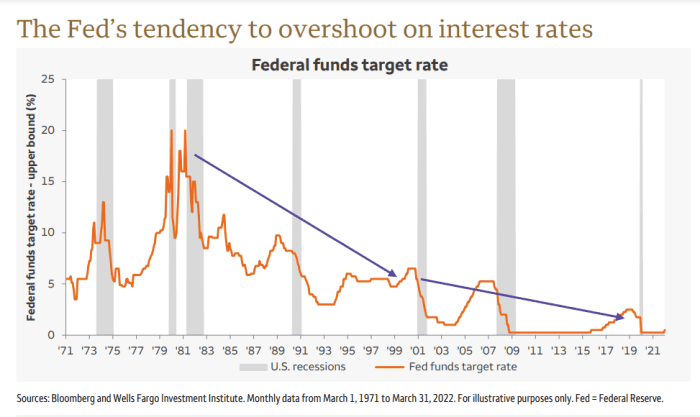

Back in the early 1980s, the federal funds target rate shot up to nearly 20% from a low of around 5% (see chart), as former Federal Reserve Chairman Paul Volcker moved to dramatically increase the policy rate to bring down long-term inflation, even though it landed the economy in a recession.

But 50 years of data shows a far more constrained upper limit for the benchmark rate than in the Volcker era before the economy falters. The below chart shows its lower trajectory since the 1980s.

The threshold for overshooting on rate hikes is lower

Wells Fargo Investment Institute, Bloomberg, Federal Reserve

“As the chart shows, over the past four decades, policy interest rates (outlined in orange) have topped out at progressively lower levels during Fed monetary policy tightening, eventually pushing the economy into a recession (gray shaded bars),” the Wells Fargo global investment strategy team wrote, in a Tuesday note.

“In 2000, the federal-funds rate peaked at 6.5%; in 2006, it peaked at 5.25%; and in 2018, it peaked at 2.5%.”

The Fed on Wednesday is expected to raise its policy rate by a larger-than-usual 50 basis point move, potentially marking the start of several outsized rate hikes this summer, and is planning to launch “quantitative tightening,” or allowing its balance sheet to roll off at a pace that will soon hit $95 billion a month.

Its shift to tighten financial conditions in recent months has sparked questions about what a more “neutral level” for rates looks like in the current monetary tightening cycle.

Fed officials began signaling around November that they no longer expect inflation to be “transitory” in the pandemic era. By March, Fed Chairman Jerome Powell raised the policy rate for the first time in four years, while saying inflation at 40-year highs might not return to pre-pandemic levels for several years.

More aggressive tones from the Fed on tackling high costs of living has led to sharp rates volatility this year, with the benchmark 10-year Treasury yield TMUBMUSD10Y,