As the painful first half of 2022 ends, many income investors are hoping for some sort of relief. Many dividend stocks have seen their yields creep subtly higher in recent months as their share prices slowly trended lower.

For income investors, the current environment has been quite hostile to dip-buyers.

We’ve suffered quite a few short-lived bear market bounces this year. Many more are sure to follow.

Though the likelihood of a V-shaped recovery is diminishing with every swift move lower, there are still plenty of oversold stocks out there overdue for a relief bounce.

In this piece, we’ll use the TipRanks Comparison Tool to evaluate three dividend stocks that Wall Street still views as “Strong Buys.”

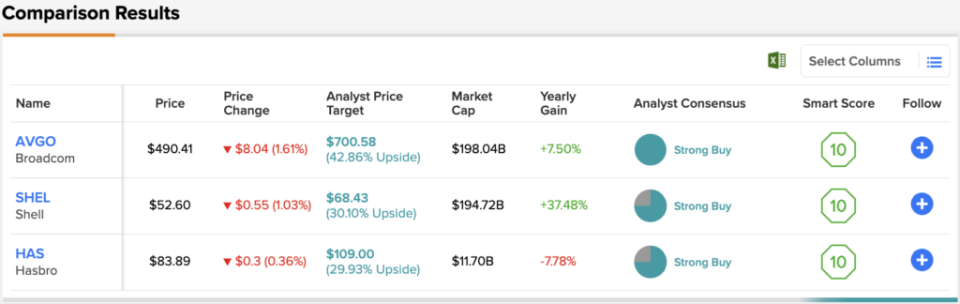

Broadcom (AVGO)

Broadcom stock is a designer and developer of semis and associated software. The chip stock plunge has been brutal to the $195 billion firm, which is now off 27% year-to-date.

The company recently agreed to acquire virtualization software company VMWare, in a deal worth $61 billion. Such a deal bolsters Broadcom’s software presence, and given the timing of the deal (after a sizable decline in tech stocks), there’s a good chance that Broadcom walked away with a bargain. Add potential synergies into the equation, and the VMWare deal is one that should be applauded by investors.

Despite Broadcom’s diversification into software via M&A, the company is still subject to the ups and downs of the semi space. Though chip demand remains incredibly robust to date, there’s no telling what a severe recession could entail for the chip maker.

On the one hand, networking chip demand seems to be on the uptrend, thanks partly to the resilience of the enterprise, who’s still more than willing to invest in the digital transformation trend. On the other hand, it’s difficult to gauge where demand will be at year-end if further evidence of an economic slowdown materializes.

If demand diminishes rapidly, any supply-chain ramp-up in response to the semi shortage could lead to discounting down the road. Over many quarters, chip demand has been high, but supply is constrained. Once supply is back in order, there’s no telling where demand will be. For Broadcom, that’s a major near-term risk.

In any case, I’m a fan of Broadcom’s latest acquisition. It demonstrates that management is disciplined regarding prices they’ll pay. At writing, AVGO stock trades at 6.7 times sales and 24.3 times trailing earnings. With a 3.38% dividend yield, Broadcom seems like a great value.

It’s not often that the analysts all agree on a stock, so when it does happen, take note. AVGO’s Strong Buy consensus rating is based on a unanimous 13 Buys. The stock’s $700.58 average price target suggests a considerable upside of ~47% from the current share price of $477.84. (See AVGO stock forecast on TipRanks)

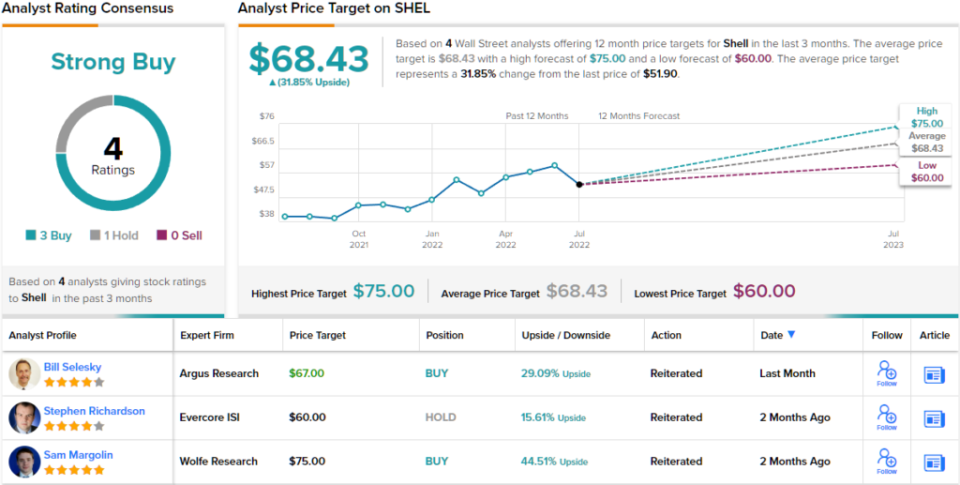

Shell (SHEL)

Shell is an oil supermajor that finally slipped into a correction after running with the energy bulls for over a year. Shell is a British firm with a simplified share structure, and a juicy 3.5% dividend yield following the latest pullback.

As oil prices creep higher again, it’s tough to count out the energy giant as it looks to make the most of its oil and gas windfall. Over the long run, Shell is ready to transition into renewables, with an energy-as-a-service model that reacts accordingly to the times.

Indeed, renewables are the future, and Shell wants to be relevant in such a future. In the meantime, it’s all about the upstream and marketing segments, which are still heavily influenced by the price of oil. As upstream slowly winds down production over the years, Shell may not be the go-to play to play a “higher for longer” type of environment.

In any case, the LNG (liquefied natural gas) business is an excellent transitionary energy that can help Shell slowly reduce its carbon emissions over the decades. With a low 0.7 beta and a modest 9.4 times trailing earnings multiple, Shell is a great stock to hedge your bets.

The 4 recent analyst reviews on this energy company break down 3 to 1 in favor of Buys over Holds, and support the Strong Buy analyst consensus rating. Shares are trading for $51.90 and the average target of $68.43 implies an upside of ~32%. (See SHEL stock forecast on TipRanks)

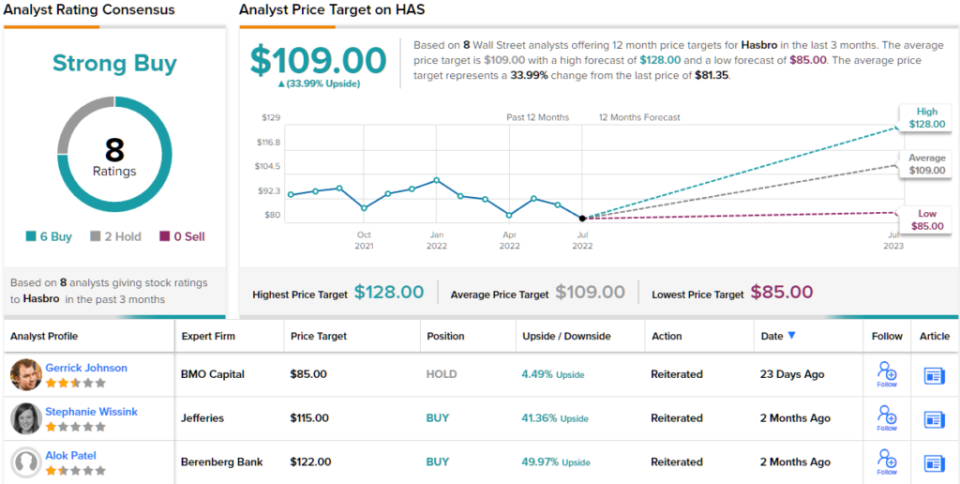

Hasbro (HAS)

Hasbro is a toy company that’s slid about 20% year-to-date. The stock never regained its pre-pandemic highs. Now that we’re talking about a recession, the stock has been downtrending again. While it’s unlikely that Hasbro will revisit 2020 lows, it seems like a consumer recession could weigh heavily on holiday demand. For such a seasonal stock, recent macro headwinds are not encouraging.

Still, analysts are upbeat, with a “Strong Buy” rating. The stock is holding its own rather well through the recent wave of supply-chain disruptions. Just because the supply side is on the right track does not mean demand will remain robust going into year-end. Further, a continuation of COVID headwinds could also weigh heavily.

Though digital games and other technologies could steer spending away from toys, I do think there’s no reason why physical toys and games can’t co-exist. They have for years, after all.

For now, the retail stalwart is a low-cost income play. At writing, the stock trades at 1.8 times sales and 28.2 times trailing earnings, with a 3.34% dividend yield.

Overall, HAS stock has picked up 8 recent analyst reviews, which break down to 6 Buys against 2 Holds, for a Strong Buy consensus rating. The shares are trading for $81.35, and their $109 average price target indicates ~34% upside for the next 12 months. (See HAS stock forecast on TipRanks)

Conclusion

Many analysts have been lowering the bar on price targets and ratings on stocks of late. The following three names have retained their “Strong Buy” status and are great long-term plays for yield hunters.

Wall Street expects the most from Broadcom of the three names in this piece, with more than 40% in year-ahead upside.

To find good ideas for dividend stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Read full Disclosure

, Eric Palmer, Has Just Spent US9k Buying 3.9% More Shares")