Buffett Going Big in Japan Is All About the Cash

(Bloomberg Opinion) — Is Warren Buffett running a day-trader style stock-screening operation?

It’s worth asking, because an investor cycling through a few Buffett-style metrics might have predicted his purchase of major stakes in five of Japan’s sogo shosha trading houses long before they were announced early Monday, sending shares in the companies soaring.

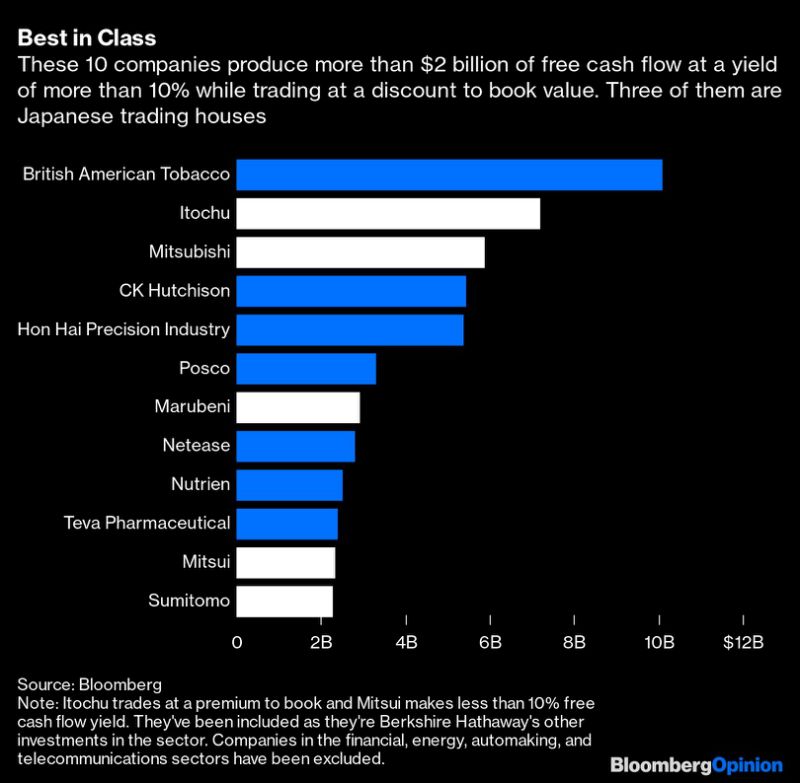

Let’s assume you’re looking for what Berkshire Hathaway Inc. has always sought out — cheap cash. Go through all the world’s listed companies and exclude those that are trading at a premium to book value, those that have free cash flow yields of less than 10%, and those that aren’t generating at least $2 billion in free cash a year.

Let’s also exclude energy companies and automakers — both going through major and unpredictable upheavals at the moment — as well as telecommunications, a sector for which Buffett has historically shown little enthusiasm. Leave out financial services, too, which already make up a pretty hefty chunk of Berkshire’s portfolio. What’s left?

Believe it or not, three of the ten businesses worldwide that meet those criteria are Japanese trading houses Mitsubishi Corp., Marubeni Corp. and Sumitomo Corp. — all companies where Berkshire has built up a roughly 5% stake over the last 12 months. Of the remaining two investments, Mitsui & Co. comes in a little weak on free cash yield and Itochu Corp. a little rich on book value, but both look close enough to match the general investment theme.

Berkshire Hathaway announced that its “intention is to hold its Japanese investments for the long term,” and the attraction of the sogo shosha isn’t hard to discern. Since their origins in the postwar keiretsu system of loosely connected business empires, they’ve made money as the glue holding Japan’s economy together, taking a cut from a Berkshire-style array of investments in raw materials, finance, transport, machinery and consumer products.

One likely reason these companies haven’t previously attracted interest from Omaha is that they’ve also traditionally been low-margin, cash-poor, debt-heavy, and more concerned with the interests of their corporate siblings than their shareholders.

As my colleague Anjani Trivedi has written, that has started to change over the past decade as leverage plummeted and the management plans guiding their activities moved from hazy strategic promises toward harder financial benchmarks, such as free cash flow and return on equity.

Several of the trading houses even have pledges on the share of profits to be paid out as dividends which, while low by international standards, are far higher than sogo shosha investors have come to expect. Those payouts translate into decent yields, too, given the low valuations the market has put on the underlying businesses:

That poses an interesting parallel to how corporate Japan has evolved, especially under the leadership of outgoing Prime Minister Shinzo Abe. As my colleagues Daniel Moss and Noah Smith have written, the premier’s tenure has seen a remarkable turnaround for an economy that many had written off as entering its dotage. Since Abe resumed office in 2012 after a five-year hiatus, Tokyo’s Topix index has outperformed every broad global stock benchmark except the S&P 500 and, in recent months, China’s CSI 300.

Once upon a time, Japan’s trading houses were like Berkshire Hathaway without the focus on shareholder returns. Now that they appear to have finally gotten the value investing religion, why wouldn’t Warren Buffett invest in them?

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

David Fickling is a Bloomberg Opinion columnist covering commodities, as well as industrial and consumer companies. He has been a reporter for Bloomberg News, Dow Jones, the Wall Street Journal, the Financial Times and the Guardian.

bloomberg.com/opinion” data-reactid=”45″>For more articles like this, please visit us at bloomberg.com/opinion

Subscribe now to stay ahead with the most trusted business news source.” data-reactid=”46″>Subscribe now to stay ahead with the most trusted business news source.

©2020 Bloomberg L.P.