Yields are in the rise again on Thursday as President Joe Biden plans to sign his $1.9 trillion covid-19 relief bill later this week after clearing the final congressional hurdle.

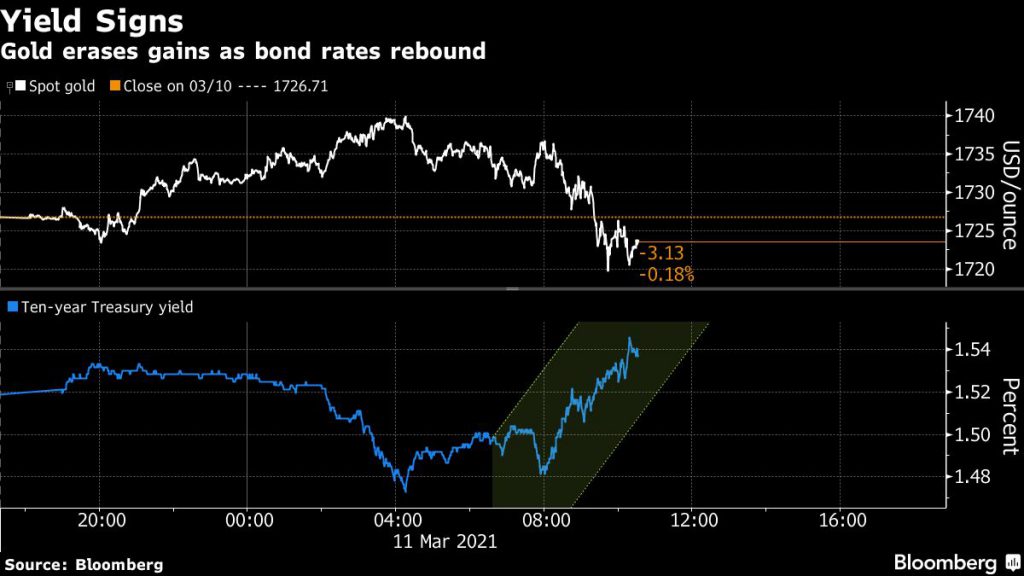

Rising yields have played havoc with the price of gold, which touched an all-time high in August. Rates have climbed as increased economic aid stokes inflation concerns, hampering demand for the non-yielding bullion.

Even so, money managers at BlackRock feel that gold has become a less effective hedge against moves in other assets, such as equities, as well as inflation.

Prospects for faster economic growth are also denting demand for the precious metal as a safe haven asset, sending prices down by more than 9% this year.

Data showed that applications for US jobless benefits fell below forecast to the lowest since early November, with covid vaccinations accelerating across the nation and states easing business restrictions.

“Bond vigilantes continue to view the massive Biden $1.9 trillion stimulus bill with deep dread concern, both with massive supply in the pipeline as well as inflation pressures,” Tai Wong, head of metals derivatives trading at BMO Capital Markets, told Bloomberg.

“Selling in bonds is keeping yields elevated and has taken gold rather smartly off overnight highs,” Wong said.

However, while the roll-out of vaccines has seen diminishing investor interest for the traditional haven, Biden’s economic package may give a huge “tailwind” to gold in the long term, according to Commerzbank AG analyst Carsten Fritsch.

“The inflation risks are growing at the same time, as handing out $1,400 to nearly every American and topping up and extending unemployment benefits are likely to massively fuel consumption,” Fritsch said.

(With files from Bloomberg)