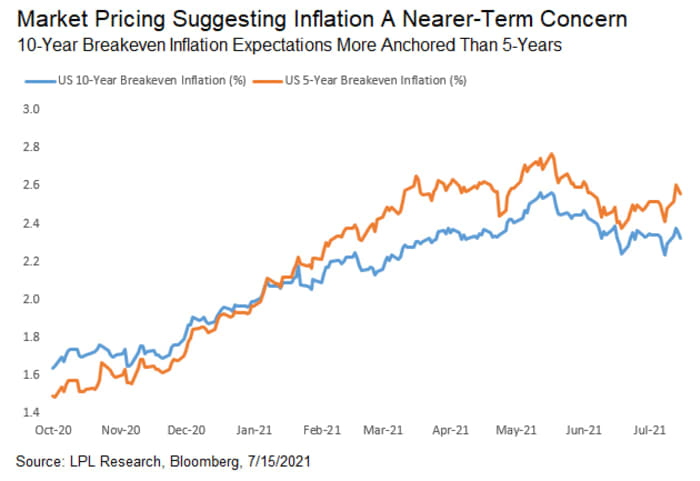

For now, the U.S. government-bond market appears to be going along with the Federal Reserve’s view that inflation will remain largely under control, even after a few months of eye-popping readings. Beneath the relatively sanguine surface, though, is an undercurrent of worry.

The concern is that 10-year Treasury yields TMUBMUSD10Y,

And if those risks come to fruition, pushing long-dated yields higher and steepening the yield curve just as in the first quarter, “that can very much lead to volatility across asset classes” as bonds sell off, credit spreads widen and stocks drop, said portfolio manager Scott Ruesterholz of Insight Investment, which manages more than $1 trillion.

Recent comments from prominent investors like BlackRock Inc.’s Larry Fink and DoubleLine Capital’s Jeffrey Gundlach only serve to underscore the worry that the market is being too complacent.

Two straight months of headline U.S. consumer price index rises at or above 5%, have parts of the financial markets unnerved. And pointed questioning by lawmakers during Fed Chairman Jerome Powell’s semi-annual testimony to Congress over the past week may have added to fears that the central bank may be misjudging the persistency of price pressures unleashed by the pandemic, even as the chairman acknowledged “a shock going through the system associated with reopening of the economy.”

A painful ride

“There is definitely a risk that the market has it wrong here,” said Mark Heppenstall, chief investment officer of Penn Mutual Asset Management, which manages $33 billion from Horsham, Pa. The CIO sees the possibility that headline consumer-price readings come in between 3% and 4% over the next six months as gross domestic product, or GDP, hits 7% to 8% for the year, pushing the 10-year Treasury back toward 2%. If higher inflation and slower economic growth play out, on the other hand, that could create “a push-pull dynamic in rates that leaves the bond market more to grapple with.”

There’s a lot riding on the outlook for bond investors over the remainder of 2021. Fixed income gets hit the hardest of all asset classes by higher inflation, which erodes the fixed value of bonds, and some investors aren’t able to ride out losses for long. “There will be some stress across other asset markets,” Heppenstall said in a phone interview. “But for long bond investors, it could be a painful ride.”

Another Fed confab looms

Investors are largely looking beyond the U.S. economic reports due for the coming week — which include housing-related data on Monday and Tuesday; weekly jobless claims on Thursday; and monthly purchasing managers’ indexes for manufacturing and services on Friday. They are focused instead on the Fed’s July 27-28 meeting in Washington, where policy makers are likely to continue their discussions of tapering bond purchases while adopting what Powell calls a more “humble” mindset on inflation.

Fed officials will be in a traditional blackout period for speeches in the coming week, leading up to that gathering.

Inflation prognostication

Meanwhile, a number of forecasters are already bracing for months of elevated price readings far above the Fed’s 2% target. Economists at Fannie Mae forecast consumer prices will stay around 5% on a year-over-year basis through the end of 2021. Those at Barclays Plc expect headline CPI to come in at 6% year-over-year in December, while Wells Fargo & Co. expects a 4% rate for the entire year — meaning that readings should continue being around 5% through the end of December.

Insight Investment’s Ruesterholz sees the likelihood of inflation continuing to come in above 3% until the second quarter of next year amid strong U.S. economic growth, before dropping back down to 2.25% to 2.5% by the end of 2022. That’s because price pressures from the reopening of hotels, increased consumer travel, and used-car sales should ultimately dissipate, while disrupted supply chains will likely “repair themselves,” the New York-based portfolio manager says.

Ruesterholz says Insight is investing in “high-yield, growth-sensitive assets” that are lower in credit quality and in collateralized loan obligations, or CLOs, and that he sees Treasury Inflation-Protected Securities, or TIPS, as an “interesting” way to play a higher-inflation scenario.

“We have to be cognizant that the forces keeping inflation elevated have been much stronger than anticipated, and we run the risk that the longer that happens, the more likely inflation is to bleed into other categories, investor psychology, and expectations,” he says.

The equities outlook

Last week, the Nasdaq Composite Index COMP,

In other words, in absolute terms, neither growth stocks, highlighted in the technology-laden Nasdaq, or the value sector, reflected in the Russell, are performing well in July.

What is working? The largest of the large are outperforming, thus far, with the Nasdaq Composite Index COMP,

“The S&P 500 is up 4% since June 3rd, but ~80% of that move can be attributed to the largest 5 stocks,” wrote Larry Adam, CIO at Raymond James’s wealth management unit, in a weekly research report.

That said, Adam said that he isn’t overly worried about the narrow breadth of winning stocks.

“Narrowing breadth is a sign of internal weakness and can sometimes precede pullback periods. We are mindful of this, but not overly concerned given the strong intermediate-term technical backdrop along with the market’s proclivity

for sector rotation latel,” he wrote.

Peak earnings?

FactSet Research’s John Butters says 85% of S&P 500 companies have reported a positive earnings-per-share surprises for the second quarter thus far.

“If 85% is the final percentage, it will mark the second-highest percentage of S&P 500 companies reporting positive EPS surprises since FactSet began tracking this metric in 2008,” he wrote on Friday.

He said the blended earnings growth rate, including actual results and estimates, for Q2 2021 for the S&P 500 is 69.3%, which would mark the highest year-over-year earnings growth reported by the index since Q4 2009 (109.1%), if figures hold.

Adam says that better-than-expected quarterly results from American companies are “attributable to the surprising resiliency of the US economy; however, as the reopening is fully realized, much of the uncertainty clouding analysts’ estimates will subside and so will the magnitude of the earnings beats.”

Raymond James will be looking for more guidance from CEOs and CFOs on the on how things are shaping up for the coming three-month period and the full year.

EARNINGS REPORTS DUE JULY 19-23

MONDAY: IBM, Tractor Supply, JB Hunt

TUESDAY: Netflix, Chipotle

WEDNESDAY: Coca Cola, United Airlines, Johnson & Johnson, Verizon, Texas Instruments, eBay, Anthem, Baker Hughes

THURSDAY: Intel, Snap, Twitter, American Air, AT&T, Domino’s, Biogen, Abbot, Equifax

FRIDAY: American Express, Schlumberger