In the view of the experts at CSIRO, such models ignore the dynamics of materials flows on a global scale and the expected changes in underlying technologies.

“Metal flows are complicated and dynamic,” the report reads. “Metals can be locked-up for decades in durable consumer goods. Product life spans differ. Uptake rates of technologies vary under different policy settings. Technologies such as EV batteries may enter second-life applications like home or grid energy storage. All of these factors interact to create the aggregate demand picture. Common economic modelling methods do not provide adequate nor coherent accounting of these physical factors ”

In the view of the team led by Jerad Ford, head o CSIRO’s critical energy metals mission in development and co-author of the paper, more accurate information can be obtained by using a tool like the Physical Stocks and Flows Framework (PSFF), which enables researchers to keep track of many physical variables and the complex dynamics that emerge when they interact with each other.

According to CSIRO, unsophisticated models based on current supply levels and basic recycling rates are promoting many mischaracterizations of the real opportunities in both metal mining and recycling

The PSFF is an integrated modelling and accounting method to track the dynamics of metal supply and demand at a global scale over long timescales. The tool helps develop scenarios so users can explore key questions such as technological change or recycling recovery rates, that will impact the demand and supply of metals. This capability can yield powerful and often counter-intuitive insights.

Using the PSFF, Ford’s group explored the behaviour of nickel, cobalt and lithium under three scenarios. The first one is the base scenario, which assumes that internal combustion engine vehicles (ICEVs) continue to comprise 98% of the global fleet, with 2% EVs, and estimates the same rates of increased light-weighting for all vehicles and changes in battery chemistries for the small number of EVs it does include.

The second scenario is the standard scenario, which is meant to represent a prospective future trend in the makeup of passenger car fleets and assumes moderate rates of change when it comes to the substitution of EVs for ICEVs in new car sales; shifts in dominant EV battery chemistries away from Co-intensive lithium-nickel‑manganese-cobalt-oxide (NMC) variants; increases in recovery efficiency from recycled end-of-life (EOL) products, and light-weighting of both ICEV and EV components, excluding the battery.

The third proposal is the rapid EV uptake, battery evolution, and light‑weighting scenario has identical settings to the standard scenario except that the substitution of EVs for ICEVs happens more rapidly (ICEV sales end globally by 2038 rather than 2050); accelerated change in dominant EV battery chemistries towards lower-Co NMC and lithium-iron-phosphate (LFP) is assumed, and light-weighting of vehicles is pursued more aggressively.

Finally, the standard scenario with battery second life has identical settings to the standard scenario, except that 60% of EOL batteries go on to serve in a second life prior to disposal/scrappage/recycling.

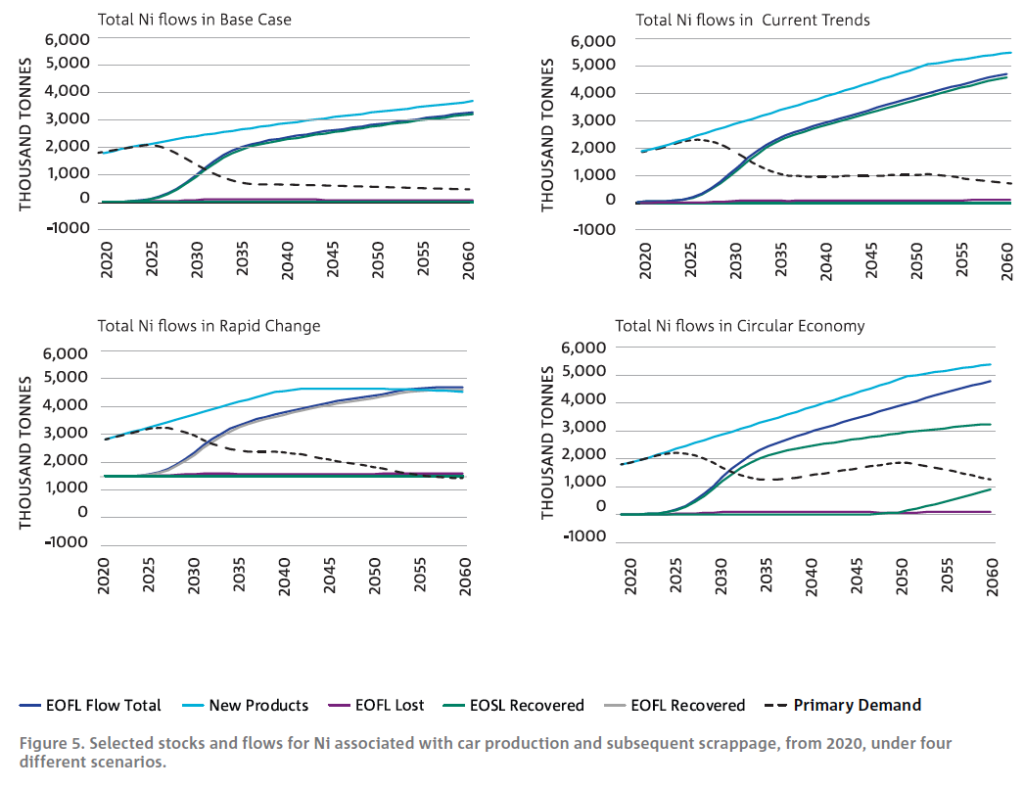

Nickel

For nickel, the report found that under the base case scenario where ICEVs continue to totally dominate personal car fleets, in little more than a decade the return flows of secondary Ni begin to supply most of the Ni required for new production.

“Primary Ni settles into a near steady-state at the relatively low (~500,000 tonnes) level, which is sufficient to fill the secondary Ni deficit driven by the growing total demand for vehicles,” the dossier reads.

Under the standard current trends scenario there is a broadly similar pattern for primary Ni demand, but with the steady-state establishing itself at a much higher level for several decades. This is driven by the higher Ni intensity of EVs, as they replace an increasing proportion of ICEVs. Once the substitution of EVs for ICEV is complete, by 2050 there is a second decrease in primary demand as return flows from scrapped end-of-first-life (EOFL) vehicles close the gap with Ni required for new products.

In the scenario for accelerated technological change, on the other hand, the earlier years appear more bullish for nickel demand but soon evolve into one that is worse for primary Ni producers over the longer term. The trajectory could reflect a real‑world scenario where high early demand for Ni drives prices higher, incentivizing moves to less Ni-intensive battery technologies such as LFP, and leading ultimately to low-to-negative primary Ni demand in later years.

The circular economy scenario illustrates the large and long-lasting effect that diverting 60% of EOL EV batteries to a second life could have on primary nickel demand. This one change in scenario assumptions compared to current trends leads to primary Ni demand settling at levels of a factor of two to four times higher for several decades, until the batteries diverted to a second life become available for scrappage in significant numbers several decades later.

“This is a stark illustration of the importance of the second life issue to primary producers, and the potential stake they could have in encouraging and facilitating it,” the document states.

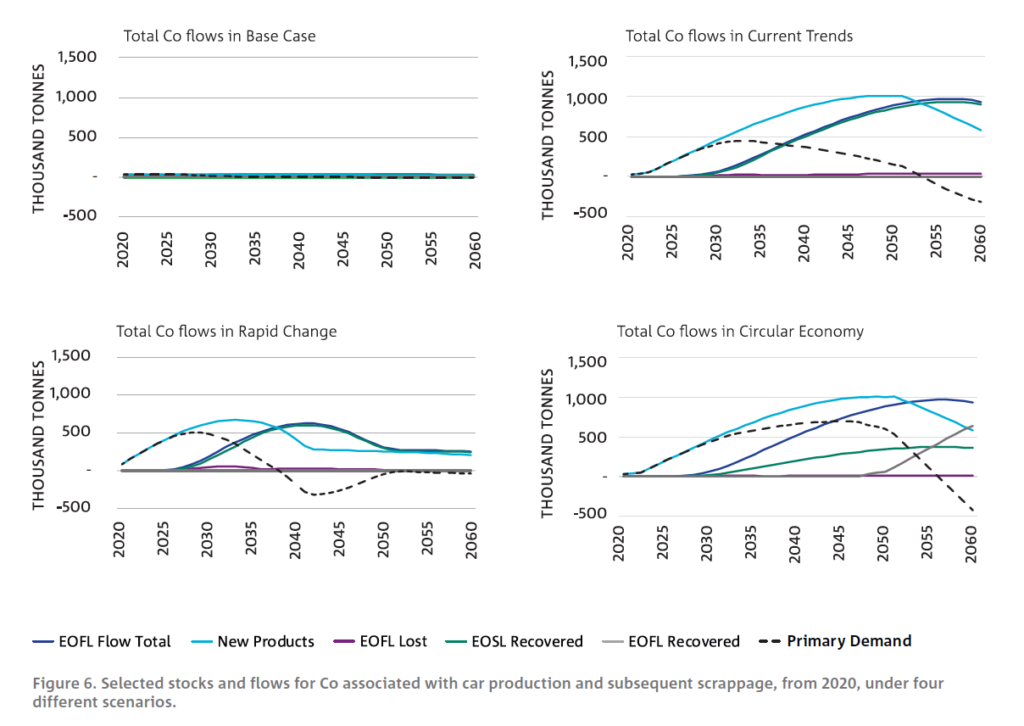

Cobalt

Under the current trends scenario, ongoing substitution of EVs for ICEVs produces rapid growth in cobalt demand by the mid-2020s, to levels several times higher than current total global production.

However, a move towards lower-cobalt formulations for NMC batteries slows this demand growth appreciably from around 2040, augmented by some shift towards non-NMC chemistries, but demand for new products continues to increase through to 2050.

Yet, effective recycling ends any boom in primary cobalt demand by the early 2030s.

“When the additional demand driven by substitution for ICEVs ends in 2050, the return flows from retiring older, high‑Co batteries quickly drives primary demand negatively,” the dossier reads. “The rapid change scenario shows how cobalt miners could be misled by the high demand trend early in an accelerated technology shift scenario. Primary demand peaks in under a decade, turning strongly negative in less than two decades.”

Accordign to CSIRO’s experts, the scenario described is not particularly radical, it simply reflects earlier substitution of EVs (completed by 2038) combined with a more rapid shift to low-Co battery chemistries.

“Comparing circular economy to current trends shows how central the single variable of second‑life usage ratios could be to the prospects of primary Co producers. Rather than current trend’s brief boom followed by decades of decline, under circular economy, the outlook for primary Co demand spans several decades, at three to five times current global demand,” the researchers found.

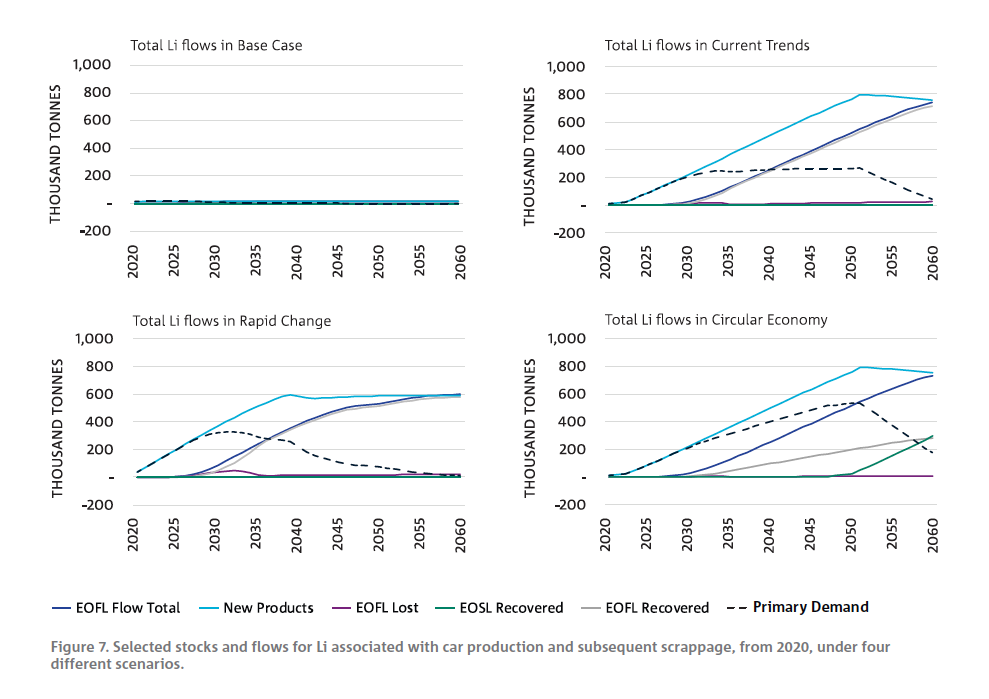

Lithium

According to CSIRO, since lithium remains central to most of the main battery chemistries being considered over the long term for use in EVs, the current trends scenario shows ongoing stable primary demand for the metal over the full period when EVs are substituting for ICEVs.

“Primary demand only goes into serious decline when demand for use in new products peaks, and lagging return flows from EOFL vehicles can subsequently begin to catch up,” the report states.

In the rapid change scenario, the accelerated uptake of EVs brings demand for lithium forward, until the substitution is complete by 2038, at which point, secondary lithium supply begins to rapidly catch up with plateauing demand from new products, driving primary lithium demand into a second, prolonged phase of decline.

“The modest declines in primary demand prior to that point are driven by changing battery chemistry shares. While Li is used in all batteries, the different chemistries have differing Li intensities per kilowatt-hours (kWh) stored,” the paper points out.

As with both Ni and Co, the circular economy scenario shows how important the viability of a second life for EV batteries will be for understanding the trajectories of primary demand and for the expansion of recycling capacity required to deal with EOL batteries.