On Tuesday, we learned U.S. employers had a record 11.5 million job openings as of March. That’s arguably the clearest sign that the economy is booming, as hiring workers isn’t cheap and most employers would only do it if they didn’t already have the staff to keep up with demand.

Currently, there are just 5.9 million people who are unemployed. In other words, there are nearly two job openings per unemployed person. The mismatch means that workers have a lot of options, which means they have a lot of leverage to ask for more pay. Indeed, employers are paying up at a historic rate.

But booming demand, record job openings, and higher wages… are bad?

The Federal Reserve and many in the economics profession are not putting it so bluntly. But that’s effectively their message.

The state of play: Demand for goods and services has been significantly outpacing supply,1 which has been sending inflation to decades-high rates. This is partly due to the fact that higher wages mean higher costs for businesses, many of which have been raising prices to preserve profitability. Ironically, these higher wages have helped bolster the already-strong finances of consumers, who are willingly paying up and thereby essentially enabling businesses to keep raising prices.

It’s important to add that this booming demand has been bolstered by job creation (i.e., a phenomenon where someone goes from earning nothing to earning something). In fact, the U.S. has created a whopping 2.1 million jobs in 2022 so far.

The Bureau of Labor Statistics has a metric called the index of aggregate weekly payrolls, which is the product of jobs, wages, and hours worked. It’s a rough proxy for the total nominal spending capacity of the workforce. This metric was up 10% year-over-year in April and has been above 9.5% since April 2021. Before the pandemic, it was trending at around 5%.

This combination of job growth and wage growth has only been exacerbating the inflation problem.

And so the best solution, at this point, seems to be to tighten monetary policy so that financial conditions become a little more challenging, which should cause demand to cool, which in turn should alleviate some of these persistent inflationary pressures.

In other words, the Fed is working to take the legs out of some of the good news coming from the economy because that good news is actually bad.2

The Fed moves to trim ‘excess demand’ ?

In a widely-anticipated move, the Fed raised short-term interest rates on Wednesday by 50 basis points to a range of 0.75% to 1.00%. It was the largest increase the central bank made in a single announcement since May 2000.

Furthermore, Fed Chair Jerome Powell signaled the Federal Open Market Committee’s (i.e., the Fed’s committee that sets monetary policy) intention to keep hiking rates at an aggressive pace.

“Assuming that economic and financial conditions evolve in line with expectations, there is a broad sense on the Committee that additional 50 basis point increases should be on the table at the next couple of meetings,” Powell said. “Our overarching focus is using our tools to bring inflation back down to our 2% goal.“

To be clear, the Fed isn’t trying to force the economy into a recession. Rather, it’s trying to get the excess demand — as reflected by there being more job openings than unemployed — more in line with supply.

“There’s a lot of excess demand,” Powell said.

Currently, there are massive economic tailwinds, including excess consumer savings and booming capex orders, that should propel economic growth for months, if not years. And so there’s room for the economy to let off some pent-up pressure from demand without going into recession.

Here’s more from Powell’s press conference on Wednesday (with relevant links added):

It’d be a far more risky situation if consumer and business finances were stretched in addition to there being no excess demand. But that’s not the case right now.

And so, while some economists are saying that the risk of recession is rising, most don’t have it as their base-case scenario for the near future.

Is it bad news for stocks? Not necessarily.

When the Fed decides it’s time to cool the economy, it does so by trying to tighten financial conditions, which means the cost of financing stuff is going up. Generally speaking, this means some combination of higher interest rates, lower stock market valuations, a stronger dollar, and tighter lending standards.

Does this mean stocks are doomed to fall?

Well, a hawkish Fed is certainly a risk to stocks. But nothing is ever certain when it comes to predicting the outlook for stock prices.

First of all, history says stocks usually rise when the Fed is tightening monetary policy. It makes sense when you remember that the Fed tightens monetary policy when it believes the economy has some momentum.

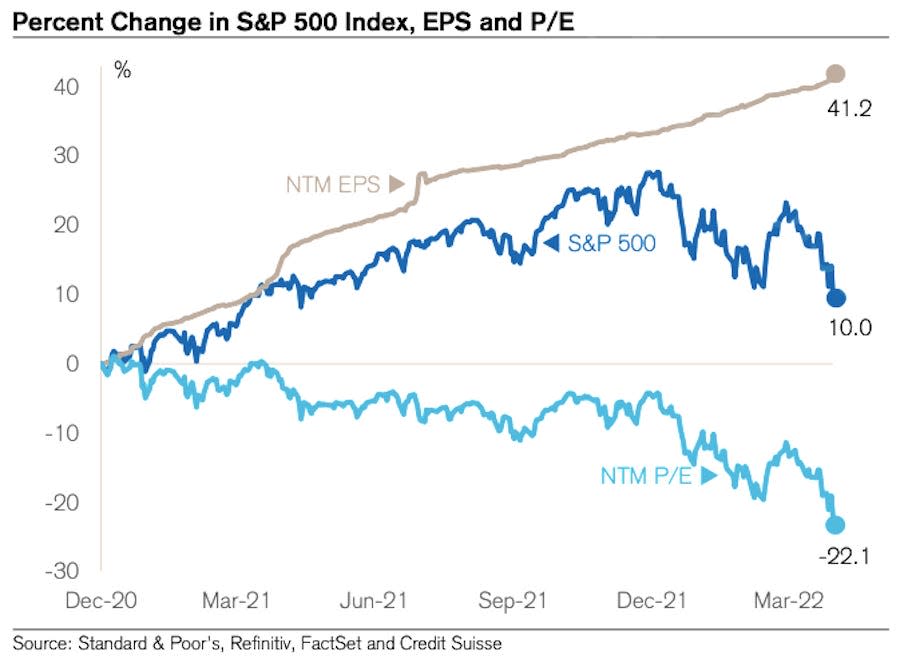

Nevertheless, the prospect for higher interest rates is definitely a concern. Most stock market experts, like billionaire Warren Buffett, generally agree that higher interest rates are bearish for valuations, like the next 12-month (NTM) P/E ratio.

But the key word is “valuations,” not stocks. Stock prices do not need to fall to bring valuations down as long as expectations for earnings are going up. And expectations for earnings have been going up. And indeed, valuations have been falling for months.

The chart below from Credit Suisse’s Jonathan Golub captures this dynamic. As you can see, the NTM P/E has been trending lower since late 2020. However, stock prices have mostly been on the rise during this period. Even with the recent market correction, the S&P 500 today is higher than it was when valuations started to fall. Why? Because, the next 12 month’s worth of earnings have essentially only been going up.

To be clear, there’s no guarantee that stocks won’t keep falling from their January highs. And it’s certainly a possibility that future earnings growth could turn negative if the business environment deteriorates.

But for now, the outlook for earnings continues to be remarkably resilient, and that could provide some support for stock prices, which are currently experience a pretty typical sell-off.3

More from TKer:

Rearview ?

???? Stocks go haywire: The S&P 500 declined by just 0.20% to round out an incredibly volatile week. On Wednesday, the S&P surged 2.99% in what was the index’s biggest one-day rally since May 18, 2020. The next day, it plummeted 3.56% in what was the index’s second worst day of the year.

The S&P is currently down 14.4% from its January 4 intraday high of 4,818. For more on market volatility, read this, this and this.

? Job creation: U.S. employers added a healthy 428,000 jobs in April, according to BLS data released Friday. This was significantly higher than the 380,000 jobs that economists expected. The unemployment rate stood at 3.6%. For more on the state of the labor market, read this.

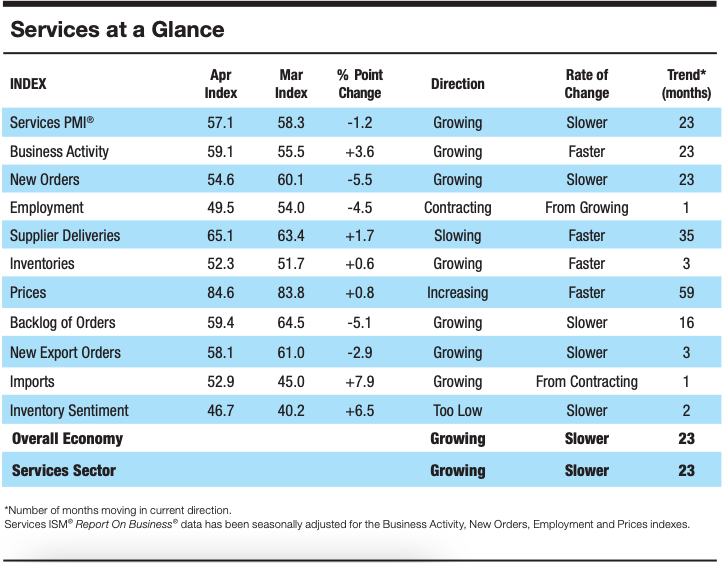

? Services activity growth cools: According to survey data collected by the Institute of Supply Management, services sector activity decelerated in April. From Anthony Nieves, chair of the ISM Services Business Survey Committee: “Growth continues for the services sector, which has expanded for all but two of the last 147 months. There was a pullback in the composite index, mostly due to the restricted labor pool and the slowing of new orders growth. Business activity remains strong; however, high inflation, capacity constraints and logistical challenges are impediments, and the Russia-Ukraine war continues to affect material costs, most notably of fuel and chemicals.”

Up the road ?

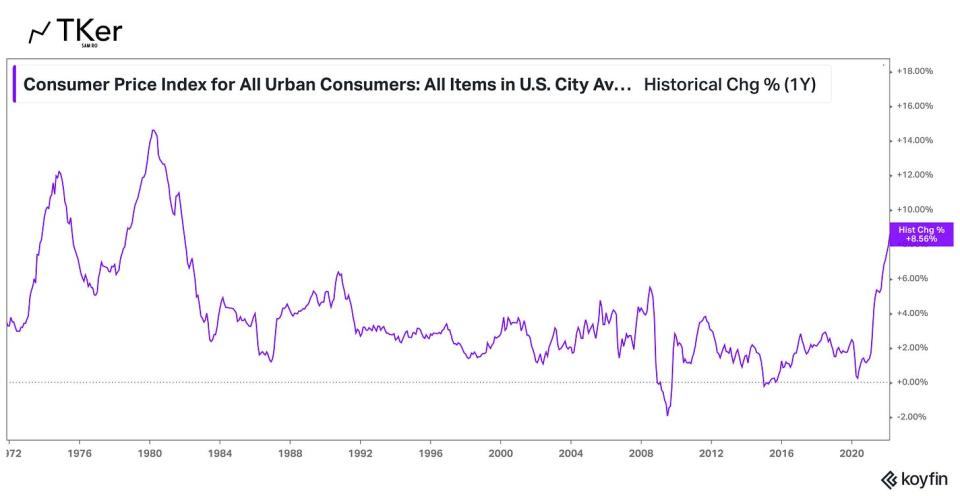

There’s no bigger story in the economy right now than the direction of inflation. So all eyes will be on the April consumer price index (CPI) report, which gets released on Wednesday morning. Economists estimate that CPI was up 8.1% year-over-year during the month, which would be a deceleration from March’s 8.5% print. Excluding food and energy prices, core CPI is estimated to have increased by 6.1%, down from 6.5% in March.

Check out the calendar below from The Transcript with some of the big names announcing their quarterly financial results this week.

1. We’re not going to get into all of the nuances of supply chain issues here (e.g., how labor shortages in the U.S., COVID-related lockdowns in China, and the war in Ukraine are disrupting manufacturing and trade). However, we know supply chain issues persist as reflected by persistently slow suppliers’ delivery times.

2. For those of you new to TKer, I’ve written a bit about how good economic news has been “bad” news. You can read more about it here, here, here, and here.

3. Investing in stocks is not easy. It means having to cope with a lot of short-term volatility as you wait for those long-term gains. Everyone’s welcome to try to time the market and sell and buy in an effort to minimize those short-term losses. But of course, the risk is missing out on those big rallies that occur during volatile periods, which can do irreversible damage to long-term returns. (Read more here, here and here.) Remember, there’s an entire industry of professionals aiming to beat the market. Few are able to outperform in any given year, and of those outperformers, few are able to continue that performance year in and year out.

Read the latest financial and business news from Yahoo Finance

Follow Yahoo Finance on Twitter, Facebook, Instagram, Flipboard, LinkedIn, and YouTube

Taxed?")

Before It Goes Ex-Dividend?")