(Bloomberg) — Suspicious minds on Wall Street can be forgiven for seeing all the hallmarks of an illiquid bear-market trap in the Tuesday stock rebound.

Most Read from Bloomberg

In recent months trading conditions in equities and bonds have gotten worse as money managers struggle to buy and sell in size without moving prices, with echoes of the 2020 pandemic disruption.

Liquidity, or the ease of trading, in S&P 500 futures is worrisome even by the standards of the Covid-spurred meltdown more than two years ago, according to JPMorgan Chase & Co. Market depth in US Treasuries is also approaching these historically dire levels in Goldman Sachs Group Inc. data.

While the trading woes in 2020 started to ease in a matter of weeks, for many Wall Street participants it feels like the problem is neverending this year as the Federal Reserve phases out the easy-money era against the backdrop of strong economic data — a recipe for cross-asset volatility.

“Market depth is not much better than it was during March 2020,” Nikolaos Panigirtzoglou, a strategist at JPMorgan, wrote in an email. “This implies that the ability of markets to absorb relatively large orders without significantly impacting the price is very low at the moment.”

These are words of caution for dip buyers who’ve returned across the board in Tuesday trading with the S&P 500 gaining as much as 1.57% while Treasuries retreated.

Everything from US stocks and global bonds to corporate credit has sunk together this year. That reflects fears that the Fed’s policy tightening campaign to cool inflation will end up hurting the US economy. Last week the main stock gauge came within 30 points of a bear market, or a 20% plunge, that’s often the precursor to recession.

With elevated cross-asset volatility, market makers become risk averse. The result is a wide mismatch between the price sellers want for assets they’re offloading and the clearing level at which dealers offer them.

Whether stock and bond gyrations are causing less liquidity or vice versa is anyone’s guess, and hard-to-trade markets is a familiar bogeyman cited by many investors whenever their returns crumble. But things are ostensibly now so bad that the Fed warned last week of the systemic risks posed by deteriorating trading conditions.

Vincent Mortier, the chief investment officer at Amundi SA, has a vivid memory of March 2020’s liquidity impasse. Things had slowed almost to a standstill, to the point where the firm had trouble selling high-quality, short-term corporate securities.

“Since that event, I told myself we need to be serious in understanding why and when bonds shifted from being liquid to being illiquid,” Mortier said in an interview. “For one day, you can handle that kind of challenge without any problem, but not when it lasts a while.”

Under its new model, Amundi determines what it would cost for a fund to liquidate 5% of its assets in a market downturn. Based on the answer, the firm assigns a stress profile to each fund and a corresponding cash buffer to cover losses from redemptions.

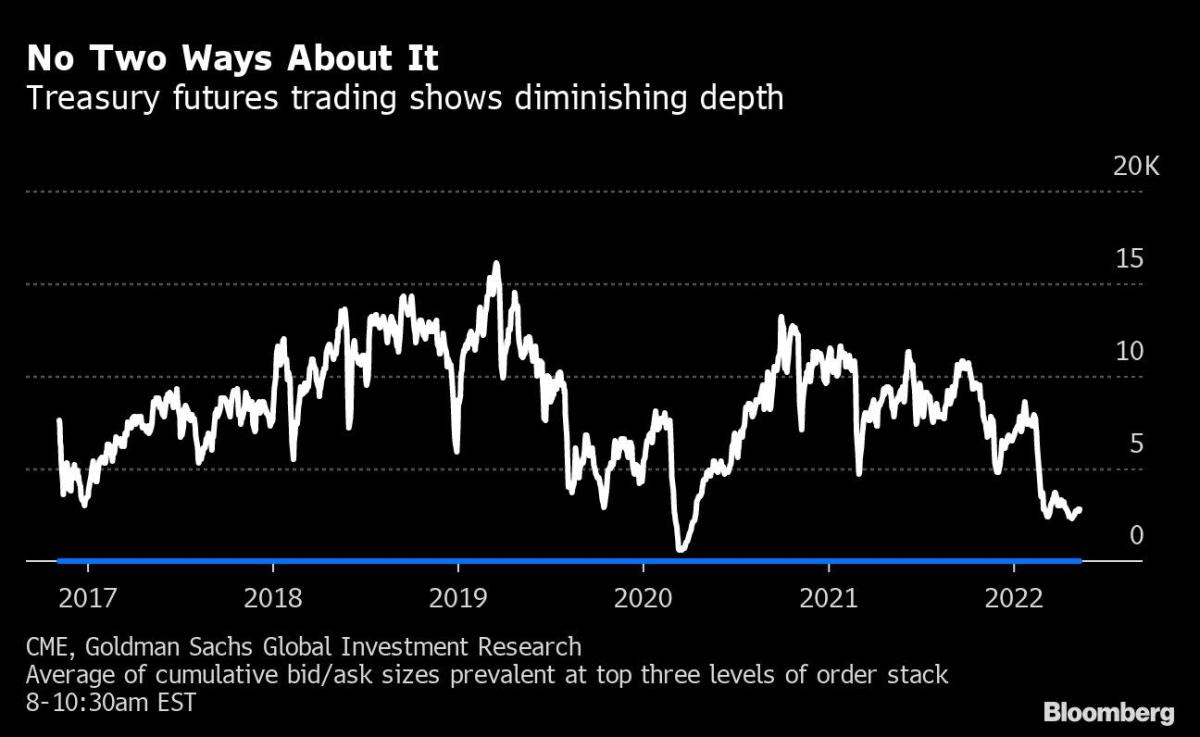

Liquidity problems are particularly acute in the world’s biggest bond market as the Fed’s hawkish turn spurs volatility.

Investment banks that once kept markets flowing have gone MIA thanks to costly limits on risk-taking imposed in the aftermath of the financial crisis. Their participation has shrunk even as the debt market has grown. Now, the Treasury market’s biggest patron, the Fed, is also retreating as it aims to jettison billions from its balance sheet.

While the plumbing of the bond market is in better shape compared to the 2020 rout, Treasury traders are securing fewer transactions at tight bid-ask spreads.

“Market depth and price impact metrics are closer to levels last seen in the midst of the Covid shock, suggesting fairly high risk of disorderly price action,” said Avisha Thakkar, a rates strategist at Goldman Sachs. “One side effect of the Fed’s absence as a backstop buyer is that there is greater risk of market fragility when shocks do arise.”

Read More: End of Easy Money Brings a $410 Billion Global Financial Shock

Read More: Treasury Market’s Weaknesses Are Laid Bare Under Strains of War

Most Read from Bloomberg Businessweek

©2022 Bloomberg L.P.