Are Ecommerce Stocks Ready for a Comeback? Analysts Offer 3 Beaten-Down Names With Big Upside Potential

Economic headwinds, in the form of rising inflation, rising interest rates, a possible collapse in the housing market, and an increasing probability of a recession have taken their toll on consumer sentiment, which in turn is taking its toll on the retail sector. Ecommerce firms, which benefited from the corona crisis of 2020, are feeling the pressure too. It seems, for now, that no one is safe.

But really? In an analysis from Stifel, analyst Scott Devitt sees a path forward for online retailers. While he acknowledges that the road is rocky, he also points out several reasons why ‘etailers’ may show gains in the second half of this year. Devitt writes, “We note that 2Q is the last quarter of difficult prior year compares, comping against stimulus checks that consumers largely received in March/April of 2021, and comps should ease as the year progresses. Once conditions begin to show stability/signs of improvement, we believe many eCommerce stocks will be proven to have been undervalued during the downdraft.”

If Devitt is correct in his breakdown of the online retail market, then current prices should mark a bottom – at least a temporary one. We may be seeing some evidence of that in the analyst reviews, as the Street’s professional stock watchers have picked out several ecommerce stocks with high upside potential, in cases to double or more on the 12-month horizon. Using the TipRanks database, we’ve pulled up the details on three of these; here they are, along with recent analyst commentary.

Farfetch, Ltd. (FTCH)

First on our list today is Farfetch, the online luxury fashion goods retailer. The company’s ecommerce platform operates to connect ‘creators, curators, and consumers’ of luxury fashion items, from jewelry to high-end shoes to accessories to clothing for men and women. Farfetch has its home base in Portugal, and operates out of offices in major global centers: London, New York, LA, Tokyo, Shanghai.

Farfetch’s shares are down 75% so far in 2022, with most of that loss coming earlier in the year. The company’s Q1 financial report was a mixed bag but providing a relatively bright spot amidst 2022’s difficulties, investors applauded a better-than-expected loss.

At the top line, revenues hit $514.8 million, whiffing on the forecast by 9% although gaining 6% year-over-year. EPS, while at an adjusted loss of 24 cents, was better than the 27-cent loss expected. The company’s gross merchandise value (GMV) showed modest growth, up 2.5% to $809.5 million. The company’s digital platform margin of 32.7% represented another relatively positive aspect, as it stayed roughly in-line with recent quarters, despite the market headwinds.

These are the basic facts behind BTIG analyst Marvin Fong’s assessment of FTCH shares. Fong notes the miss against expectations, and writes, “The drivers of the lackluster 1Q22 performance was the spread of COVID-19 in China, which caused an abrupt and severe drop in sales, and continued weakness in the markdown channel as sales there declined 17% y/y.” Getting into the stock’s positives, and its attraction for investors, Fong adds, “We believe FTCH’s anticipated ability to defend margin through cost rationalization is a small, but pleasant, surprise…. we think at [approximately] $8, the stock has overshot to the downside. We believe the current market price is valuing the marketplace at just ~2x gross profit, which we think is overly punitive for a quality e-commerce asset — we target 5x.”

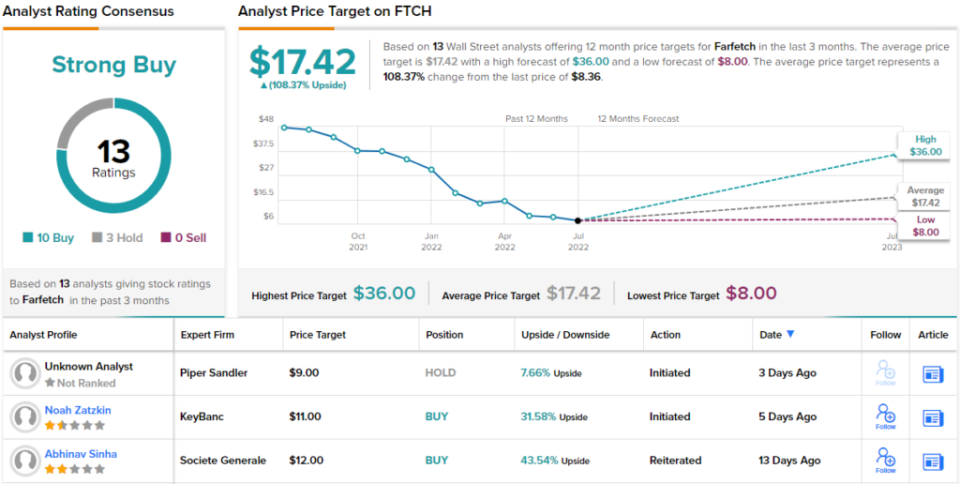

Indeed, Fong now thinks the shares are undervalued, calling the “battered” shares appealing. Along with a Buy rating, his $16 price target indicates potential for a 91% upside in the coming year. (To watch Fong’s track record, click here.)

It looks like Wall Street is on the way to being convinced of Farfetch’s upside, as the 13 recent analyst reviews do skew 10 to 3 in favor of Buy over Hold, for a Strong Buy consensus rating. The shares have a trading price of $8.36 and their average price target of $17.42 suggests a robust 108% upside in the coming year. (See Farfetch’s stock forecast at TipRanks.)

MercadoLibre, Inc. (MELI)

Next on our list, MercadoLibre, is a leader in the Latin American online retail sector. The region ‘south of the border’ tends to get overshadowed by its giant neighbor, perhaps unfairly, as Latin America has a total population exceeding 665 million, a collective GDP of $5.3 trillion, and is a major supplier of petroleum, iron ore, copper, and agricultural products. MercadoLibre, an Argentinian company trading on Wall Street, has been in business for more than 20 years, and operates in 18 countries including the regional powerhouses of Argentina, Brazil, and Mexico.

MercadoLibre posted strong numbers in 1Q22, with $2.2 billion at the top line, for a year-over-year gain of 67% when taking foreign exchange into account. In several other metrics, the company showed additional gains, including a 31% y/y gain in gross merchandise value to $7.7 billion, and an 81% y/y gain in total payment volume to $25.3 billion. In short, the company started off 2022 on a strong footing.

Earnings reflected that strength. Diluted EPS jumped y/y, from a 68-cent loss to a $1.30 profit.

Despite these clear gains, MELI shares are down 42% year-to-date. The stock has suffered from a trend of the current downturn, a move away from growth stocks and toward more defensive investments.

Covering this stock for JPMorgan, analyst Marcelo Santos believes the retail giant’s strong performance is the key, writing, “We see valuation as compelling, with shares trading at a 10yr low in terms of EV/Revs, while the company has been able to continue showing healthy growth in its key segments, and at the same time, improve monetization.”

Looking forward, Santos adds a case for continued expansion: “We expect e-commerce to continue expanding well, with GMV up 32% in local currencies during 2022E, while off-platform TPV should grow 105% y/y. Moreover, we model the gross credit portfolio expanding 125% y/y in USD terms during 2022, with consumer portfolio (including credit card) reaching 75% of total by the end of the year.”

These comments back up the analyst’s Overweight (Buy) rating on the shares, while his $1,300 price target predicts a 70% upside lying ahead in the next 12 months. (To watch Santos’ track record, click here.)

For investors seeking a stock with a firmly based Strong Buy consensus, this could be the bet. Of the 13 recent analyst reviews here, 12 have given MELI shares a Buy against a single Hold. The stock does not run cheap, with a current trading price of $763.92, and its average price target, at $1,298.46 implies 70% share appreciation in the coming year. (See MercadoLibre’s stock forecast at TipRanks.)

RealReal (REAL)

Combining both brick-and-mortar and online retail, RealReal operates as consignment resale dealer of authenticated luxury goods. Products listed on the site and offered in the real-world locations, include a wide range of sought-after brand-name goods, including accessories, handbags, jewelry, and clothing. As a consignment dealer, RealReal maintains teams of in-house experts to verify that every item sold is authentic – the real deal – whether online or in a retail location.

RealReal, like MercadoLibre above, has combined some solid financial results with a sharp decline in share value this year. The Q2 numbers won’t be reported until next month, but a look backwards shows a gross merchandise value of $1.5 billion last year, with 85% of that coming from repeat buyers, and total of $2.5 billion in cumulative commission payouts.

In 1Q22, the company saw $428 million in GMV, for a 31% y/y increase, and revenues of $147 million, for a y/y gain of 48%. The company expects these gains to hold, and has guided toward full-year 2022 GMV in the range of $2 billion to $2.1 billion; achieving that would mark a gain of one-third or more over 2021’s number.

At the same time that RealReal is posting these numbers, the company is also dealing with a fall in share value and turnover in upper management. The stock has fallen 79% this year, pushing the shares into ‘penny stock’ territory. And, the long-time CEO Julie Wainwright, who founded the company back in 2011, is stepping down, leaving RealReal in the hands of co-interim CEOs while a search for her successor continues.

Needham’s Anna Andreeva points out that the departure of Wainwright is ‘not indicative of change in strategy/fundamentals,’ and appears to be amicable – important points, as they suggests a smooth transitional period for upper management and the company in general. She writes, looking forward at the firm’s potential, “We are bullish on the circular economy’s growth potential, and we see REAL as the only luxury marketplace operating at scale… For 2Q22, we think there could be some upside to sales/GMV (we and consensus model at the mid-point of the guide) — according to our checks, both higher ticket items like handbags and lower priced (but higher take rate) apparel are moving quickly (part of going out/return to work)…”

Andreeva uses her comments to support a Buy rating on the shares, and she sets a $10 price target for the coming year, suggesting an impressive 306% upside potential. (To watch Andreeva’s track record, click here.)

While Andreeva is upbeat, not all on the Street are on the same page. This stock has picked up 9 analyst reviews recently, and they include 4 Buys – against 5 Holds, for a Moderate Buy consensus rating. The stock’s average price target of $7.13 indicates room for 189% growth from the trading price of $2.46. (See RealReal’s stock forecast at TipRanks.)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.

Share Price Increased 727%")